Trump’s Tax Deadline (Yours Too)

![]() Trump’s First Order of Business

Trump’s First Order of Business

What a whirlwind — 11 presentations in two hours and 45 minutes.

What a whirlwind — 11 presentations in two hours and 45 minutes.

From far and wide, the Paradigm Press editors converged on our Baltimore headquarters yesterday.

They unveiled their top forecasts for 2025 — the trends, the opportunities and especially the surprises.

They faced a tough crowd — their fellow editors as well as our support staff of laypeople who are much like you — open to entertaining complex ideas, but wanting them boiled down to clear takeaways.

I’m still pulling all my notes together; look for highlights on Monday.

In the meantime, it’s not too early to look ahead to one of the major economic agenda items for the Trump administration…

Beyond whatever executive orders he issues on Inauguration Day, the first order of business in Donald Trump’s second term will be the same as it was in his first — taxes.

Well, actually, the first order of business in his first term was repealing Obamacare — but that never got done, even with Republican control of the House and Senate.

But tax cuts did get done in 2017. And they came with an expiration date — year-end 2025. Barely 12 months from now.

That’s a function of the byzantine budgetary logic under which Washington, D.C., operates. Everything has to pencil out (kinda, sorta) over a decade-long time horizon. So in this instance, the only way to “recover” the “lost” revenue from this tax law was to sunset the entirety of the law after eight years.

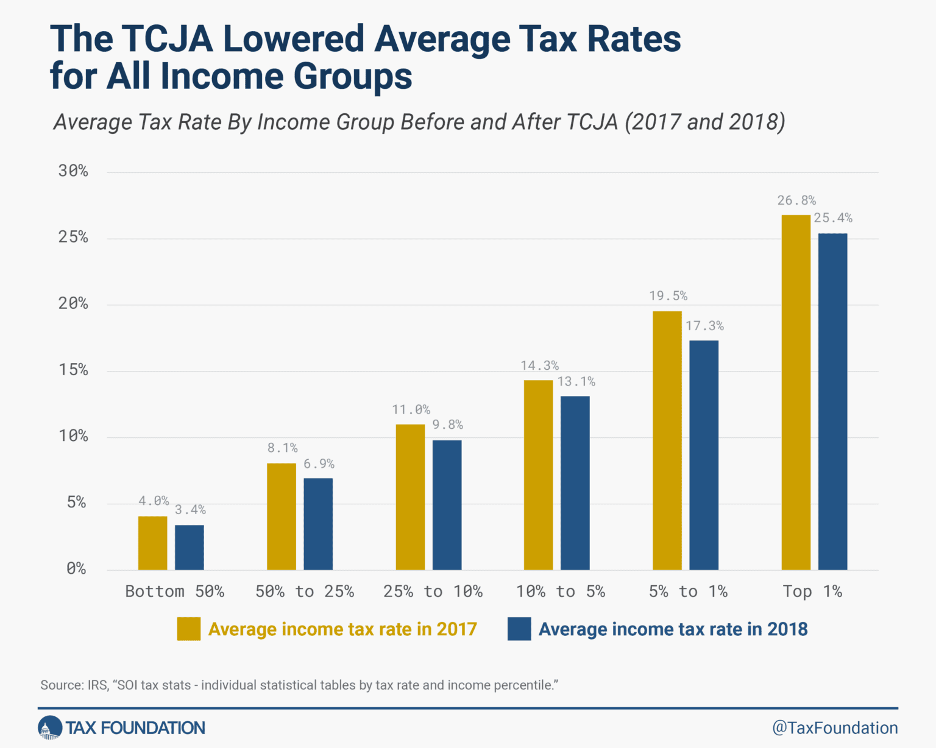

The Trump tax cuts — formally the “Tax Cuts and Jobs Act” — lowered average tax rates for all income groups, according to research from the Tax Foundation…

With Republicans in charge of both the House and Senate, those post-2017 rates are sure to stay in place now — even for folks at the top end of the income scale.

But beyond that, there are many other details to thrash out. On the campaign trail this fall, Trump said he wanted to…

- End the taxation of Social Security benefits

- Eliminate taxes on tips

- Exclude overtime pay from income tax

- Make interest on auto loans fully deductible

- Jack up the child tax credit.

One more possibility — raising the cap on the SALT deduction for state and local taxes. Republicans from high-tax blue states like New York and California have wanted this for years; Given how Trump improved his vote margin in those states between 2020 and 2024, he might be receptive.

But political realities are such that he’s not going to get everything he wants on that list.

Today, we’ll propose an alternative wish list. It has to do with a series of “gotcha” taxes that you may or may not be aware of. They’re worth bearing in mind as you get ready to prepare your taxes next spring.

Every item on the following wish list would ease the burden of inflation — which, you’ve probably noticed, has had an impact on your monthly budget in recent years.

![]() Please, Please — Repeal These “Gotcha” Taxes

Please, Please — Repeal These “Gotcha” Taxes

If Trump can’t end the taxation of Social Security benefits, the least he could do is to end the “gotcha” tax that’s built into Social Security.

First, the background. When Social Security was overhauled during Ronald Reagan’s first term, Social Security benefits became taxable income for the first time.

Since 1984, seniors have paid tax on “provisional income” above $32,000. The figure is calculated by adding up your gross income, tax-free interest and 50% of Social Security benefits.

Even though this formula came into effect 40 years ago, it’s never been adjusted for inflation. If it were, the threshold would be $96,863.

LOGO — Another gotcha tax is more recent: It affects homeowners and it came into effect under Bill Clinton.

Under the Taxpayer Relief Act of 1997, there’s an exemption on any capital gains you rake in from the sale of a personal residence — $250,000 for individuals, $500,000 for couples. (You have to have lived in the home for at least two of the last five years, and the exemption is allowable only once every two years.)

Even though this legislation was passed more than a generation ago, those thresholds have never been adjusted for inflation. If they were, they’d be $489,740 for individuals and $979,490 for couples.

And even those higher figures wouldn’t be fair — considering that home prices have risen much faster than the inflation rate.

Imagine a just-retired couple looking to downsize and sell a home where they’ve lived for the last 20 or 30 years. Ouch.

This is a reality that’s biting especially hard right now for Californians looking to move to a lower-tax locale like Arizona or Texas.

And then there’s the Obamacare tax.

Strictly speaking, it’s a Medicare surtax, but it took effect along with Obamacare in 2013. There are two main features to this surtax…

- A 3.8% levy on dividends and long-term capital gains for individuals earning over $200,000 and couples earning over $250,000

- A 0.9% levy applied to all income over $200,000 for individuals and $250,000 for couples (on top of the 1.45% Medicare tax everyone pays on every dollar of wages)

Even though these income thresholds came into effect more than a decade ago, they’ve never been adjusted for inflation. If they were, they’d be $269,960 for individuals and $337,450 for couples.

(And even with those higher thresholds, there’d still be a heckuva marriage penalty.)

One more gotcha tax — and this one even precedes the tax on Social Security benefits.

As you might be aware, you can write off investment losses on your income taxes — up to a point.

Tax-loss selling, it’s called: You sell an underperforming investment and apply the loss to reduce your taxable capital gains. If your losses are greater than the gains, you can offset as much as $3,000 of your ordinary income.

Sounds generous, you say? Not so much. Under the Tax Reform Act of 1976, this $3,000 cap took effect way back in 1978 — when Grease was the No. 1 movie and the year’s top-charting song was Andy Gibb’s “Shadow Dancing.”

Yeah, it’s never been adjusted for inflation. If it were, it would be nearly $14,500 now.

Fixing these gotcha taxes seems like a modest and doable way to take some of the sting out of this decade’s inflation — for which both Trump and Biden bear responsibility.

But before we move on, there’s one other item we need to address: We sincerely hope it doesn’t end up on Congress’ agenda, but we can’t dismiss the possibility.

See, if the Trump tax cuts are to be made permanent, the politicos are gonna have to come up with more revenue from somewhere.

![]() The End of the 401(k) Tax Break?

The End of the 401(k) Tax Break?

And that “somewhere” might be your 401(k).

After all, “Eliminating the favorable tax treatment of the 401(k) is much less painful politically than increasing taxes directly,” economist Allison Schrager wrote in a Bloomberg opinion piece earlier this year.

I’ve been following this story since the 2008 financial crisis. Back then, when the crash had already vaporized $2 trillion from Americans’ 401(k) and pension plans, I wrote at The Daily Reckoning’s website about a proposal in Congress to exclude “high income” earners from making tax-deferred 401(k) contributions.

Rep. George Miller, chair of the House Education and Labor Committee, was candid about the aim: “We’ve invested $80 billion into subsidizing this activity.” In other words, Uncle Sugar was “sacrificing” $80 billion in revenue every year for the sake of a “high-income” giveaway.

The idea never got out of committee… but it’s never gone away. Academics, think-tank types and investment bankers have all issued position papers on the topic in subsequent years — some of them suggesting that the tax breaks of a 401(k) be phased out for everyone, no matter their income.

Key point: Republicans seriously entertained this idea while writing the Trump tax cut bill in 2017.

Trump’s director of the White House National Economic Council, Gary Gohn, floated the idea.

House Ways and Means Committee chair Kevin Brady (R-Texas) appeared receptive. If it had gone through, your annual 401(k) contributions would have been capped at a paltry $2,400.

For perspective, the cap for most people that year was $18,000; this year, because the cap is adjusted for inflation, it’s $23,000.

Under the proposal, any contributions above that puny $2,400 cap were to be “Rothified.” That is, it would be treated like a Roth IRA — you’d pay taxes on it now, with the promise that the money plus any investment gains could be withdrawn tax-free in retirement.

There was just enough pushback that Trump issued a tweet promising “NO change to your 401(k). This has always been a great and popular middle class tax break that works, and it stays!”

Cohn lasted only 15 months at the White House and Rep. Brady retired at the end of 2022, so they’re not around to resurrect this proposal. But someone else might this time: Would Trump squash it down again, or would he trade it off for another concession as he pursued the art of the deal?

We’ll concede it’s a low-probability outcome. But it would also be high-impact. We’ll stay on top of it…

![]() Reliable Recession Benchmark

Reliable Recession Benchmark

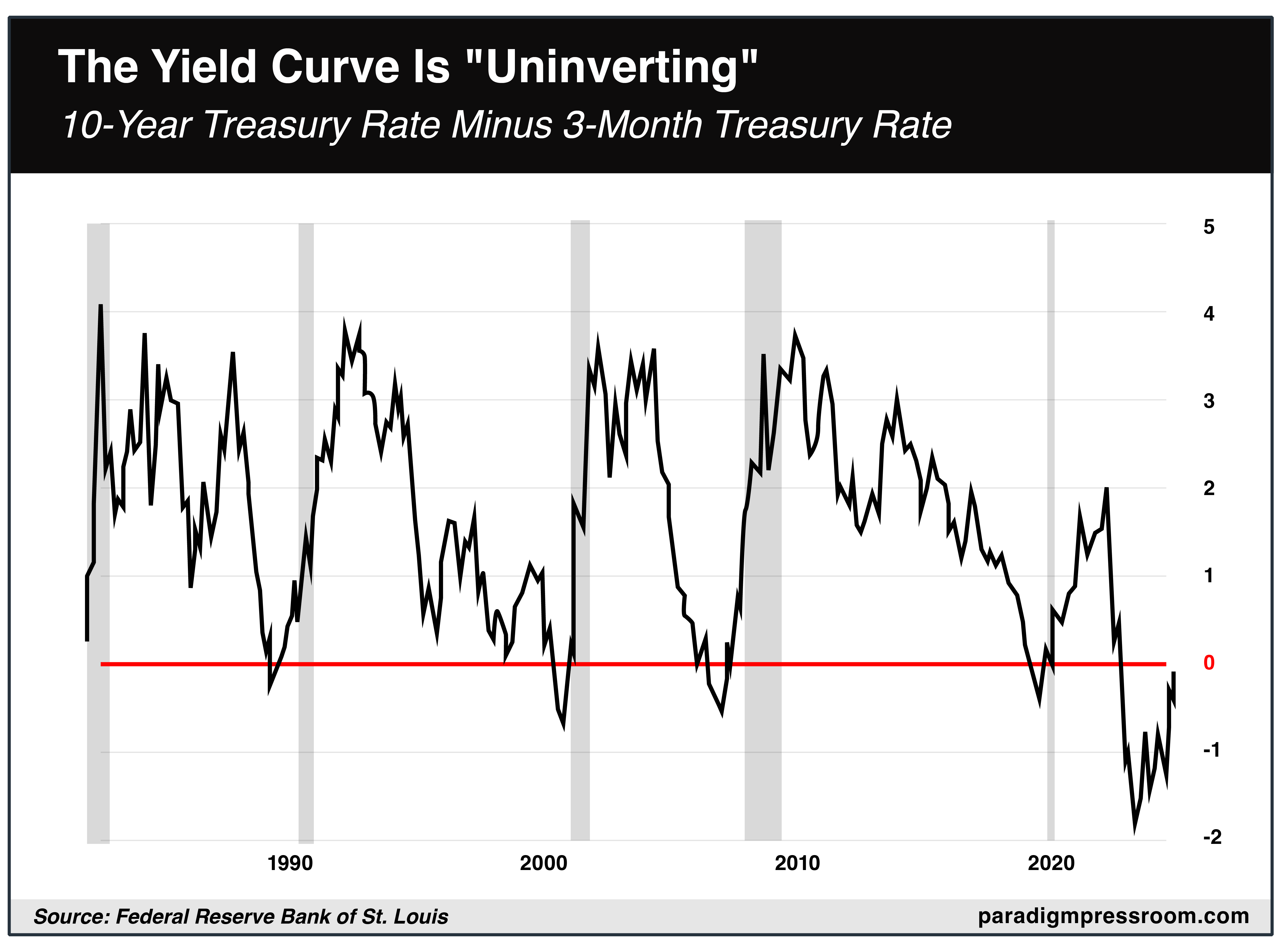

By one measure, a 2025 recession is baked into the economic cake now.

That’s because the 3-month/10-year yield curve has uninverted.

Yeah, we’d better back up in case you’re unfamiliar or you need a refresher.

Under normal circumstances, long-term interest rates are higher than short-term rates. That’s because under normal circumstances, lending money for longer stretches of time is more risky; there’s more time for something to go wrong and the borrower to default.

But on occasion, short-term rates become higher than long-term rates. When that happens lenders anticipate a higher risk of delinquency or default in the short term. Often, that risk is associated with fears of a recession. This is what’s known as an “inverted yield curve.”

There’s a lot of misunderstanding surrounding an inverted yield curve; many people think that when it inverts, a recession is imminent.

In reality, it’s when the curve uninverts that a recession is nigh.

Certainly that’s how it’s worked out with every recession going back to 1990. When the line on this chart goes back above zero, the curve has “uninverted.” Note well: The vertical gray bars are recessions.

Timing, you wonder? Here’s how it shook out with the four most recent recessions…

- The 1990–1991 recession began eight months after the curve uninverted in November 1989

- The mild 2001 recession began only two months after the curve uninverted in January

- The “Great Recession” of 2007–2009 began seven months after the curve uninverted in May 2007

- The brief 2020 COVID recession began four months after the curve uninverted in October 2019. As we’ve recounted in the past, a 2020 recession was likely in the cards even without a pandemic.

Admittedly, this is a limited data set. But there’s an average five-month interval between the time the curve uninverts and the time a recession sets in. So… next May, perhaps?

No guarantees, though: A lot of economic numbers have been scrambled in recent years by 1) the rise of work-from-home and 2) an enormous influx of immigrants, legal and otherwise. Perhaps the uninverted yield curve is one of those numbers and it no longer has the predictive value it once did…

To be sure, there’s little evidence of recession fears in the major U.S. stock indexes as the week winds down.

At last check, the Dow is flat, the S&P 500 is up slightly and the Nasdaq is up about a third of a percent.

If these numbers hold by day’s end, the Nasdaq will notch a record weekly close — but not the Dow or the S&P.

Meanwhile, commodities traders are shrugging off the risk of a sudden geopolitical blowup this weekend while the markets are closed.

Oftentimes, gold and oil traders avoid being “short” on a Friday when the world looks volatile — and that’s certainly the case today…

- According to Israeli media, the Israeli military sees the downfall of the Assad regime in Syria as an ideal opportunity to start bombing Iran. There’s almost nothing left of Syria’s Russian-made air defenses after Israel spent most of this week bombing the hell out of them. In the past, those air defenses were a formidable deterrent to Israeli bombings of Iranian targets, but no more.

- Ukraine has once again used American-provided ATACMS missiles to strike well inside Russian territory. The last time Ukraine did this, Russia unleashed its new game-changing Oreshnik missile — as Jim Rickards recounted for us yesterday. The logical response this time would be an attack on the new U.S. missile base in Poland…

And yet gold and silver are taking another beating today — gold down nearly $19 at $2,661 and silver off another 46 cents to $30.47. The HUI index of mining stocks is back below 300.

Crude is rallying, but not dramatically — up 77 cents to $70.79, the highest since before Thanksgiving.

Bitcoin’s rally back above $100,000 is holding going into the weekend.

Staying with geopolitics as we wind down the week…

![]() Comic Relief

Comic Relief

Playing off a meme we shared on Monday…

I don’t know who’s actually behind the “Iran Military” account on X, but it’s home to some first-class trolling of the Deep State!

Have a good weekend,

Dave Gonigam

Managing editor, Paradigm Pressroom's 5 Bullets

")

")