DOGE Boys Disappoint

![]() Here We Go Again

Here We Go Again

All is calm again in the stock market now that there’s a truce in the trade war… but the bond market is once more showing signs of stress.

All is calm again in the stock market now that there’s a truce in the trade war… but the bond market is once more showing signs of stress.

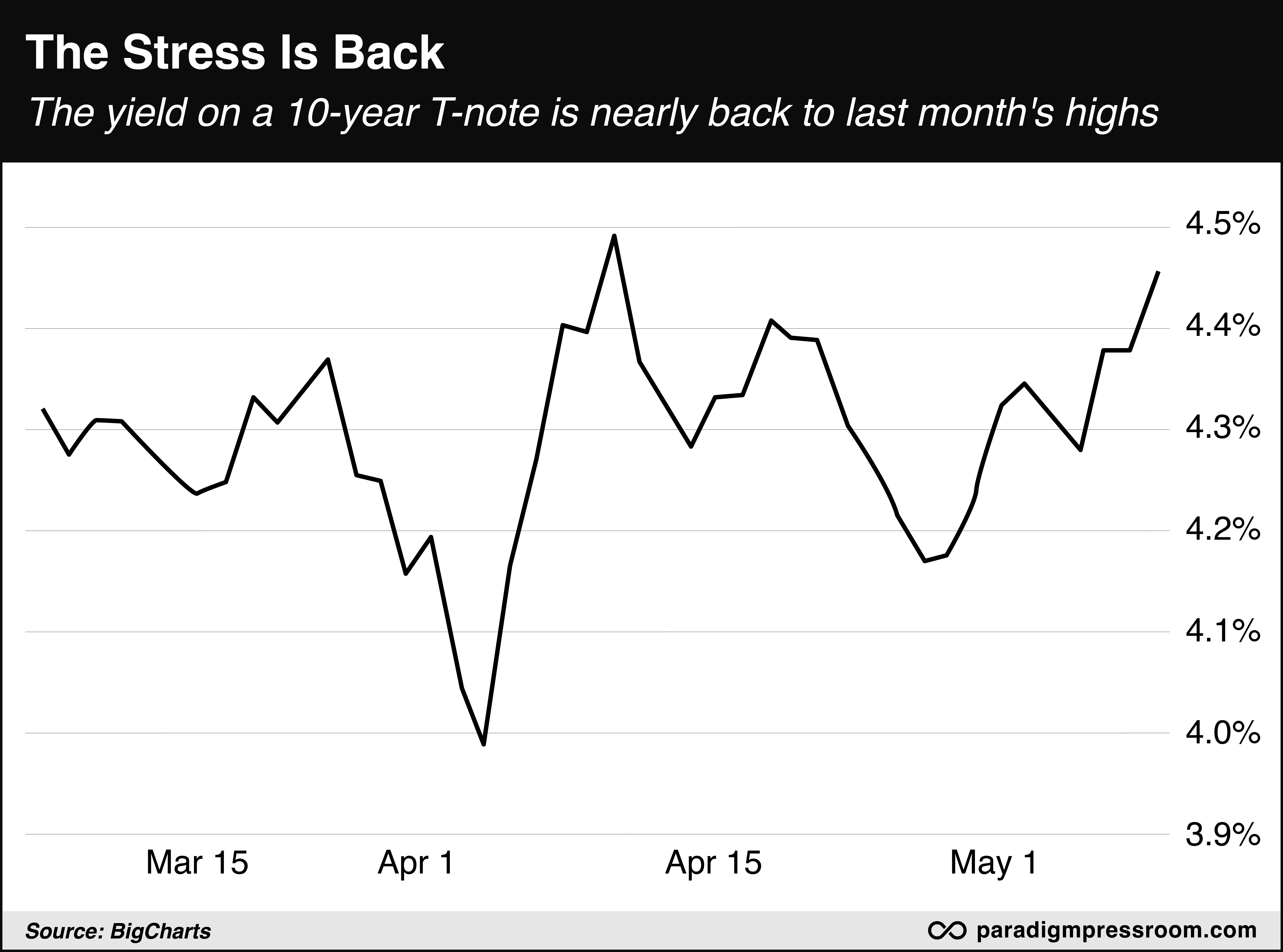

A quick refresher from last month: Bond prices collapsed, sending yields soaring, in the wake of the president’s “Liberation Day” announcement. The yield on a 10-year Treasury zoomed up from 3.99% to over 4.5% in a week — a massive disruption in bond-land.

Recall that the stock market was selling off hard at that time. Usually Treasuries serve as a safe haven. At such times, bond prices rally and yields fall. But not last month. It seems foreigners in particular were eager to dump their Treasury holdings.

The mainstream narrative was that it was all Trump’s fault with the on-again, off-again tariff uncertainty.

And while that was certainly part of the story, the trouble had been building for a while.

For one thing, the bond market is getting increasingly apprehensive about the gargantuan size of Uncle Sam’s debt. The jitters were made worse when Congress moved last month to scrap a 50-year tradition called “reconciliation” that kinda-sorta kept the growth of the debt in check.

Too, there’s lingering bad blood from when the Biden administration froze the U.S. Treasury paper owned by Russia’s central bank — even handing the interest payments to Ukraine. Dozens of foreign leaders thought, If it can happen to them, it can happen to us.

Here we go again: The yield on a 10-year T-note is up to 4.47% this morning — nearly as high as it was at the peak of the bond market freakout last month.

That’s because two things happened after we hit “send” on yesterday’s edition…

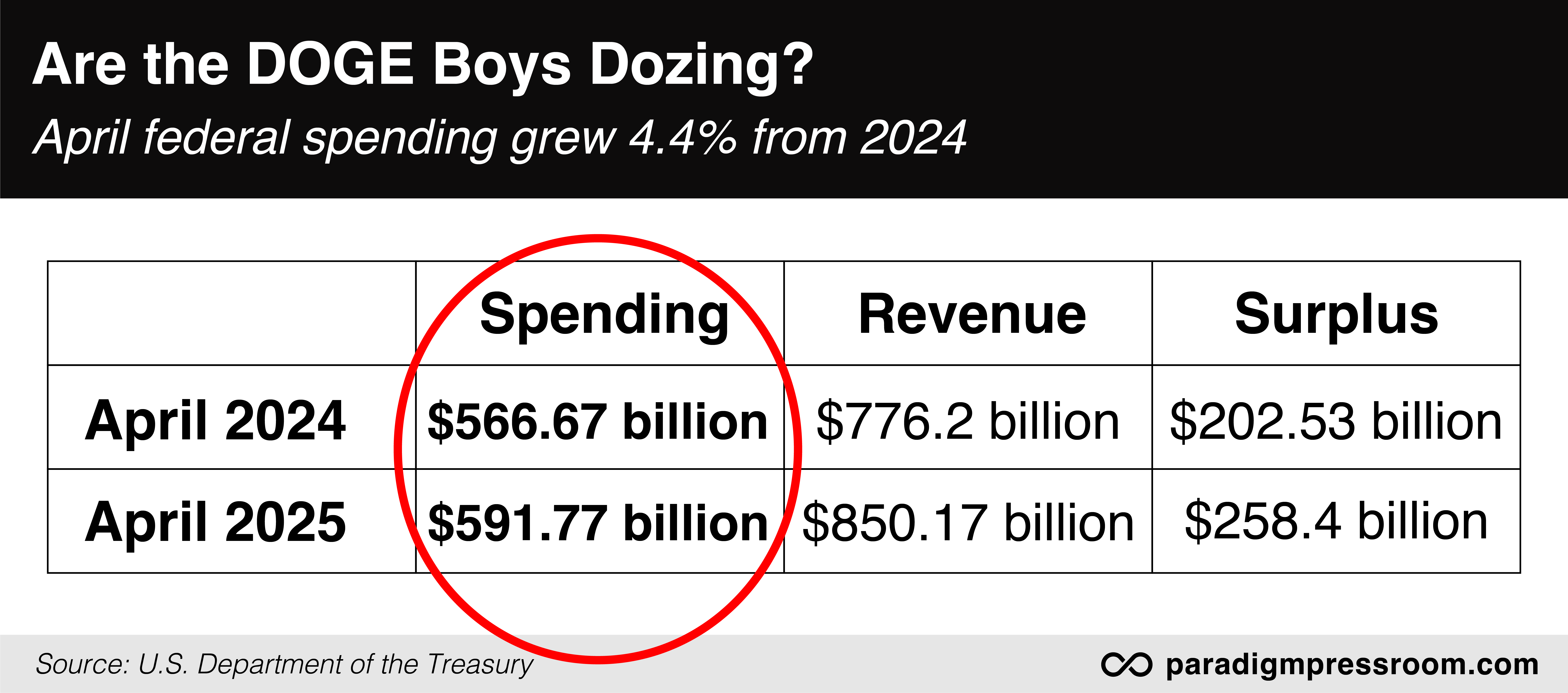

The first thing that happened is the Treasury Department issued its monthly statement of income and outflows for the month of April.

The April statement is usually an outlier: Uncle Sam records a surplus because of all those income tax payments. That’s the case for April 2025, and indeed the surplus is higher than it was in April 2024 (helped a bit by record tariff payments).

But look at the spending column. Spending was up 4.4% year-over-year. What the hell is the “Department of Government Efficiency” accomplishing, exactly?

For the first three full months of the Trump 47 administration, spending was a hair higher — about 1.2% — than it was during the same three months of 2024, when Joe Biden was handing out goodies in hopes of winning a second term.

The numbers are the numbers. And they don’t live up to the DOGE boys’ brash proclamations.

True, one month’s figures might not have been enough to move the bond market by themselves. Which brings us to the second thing that happened yesterday…

![]() Trump Tax Cuts 2.0

Trump Tax Cuts 2.0

The second thing that happened is that congressional Republicans released their big tax bill.

As we mention now and then, the 2017 Trump tax cuts expire at the end of this year. Everyone returns to Obama-era rates if Congress doesn’t act.

This bill would not only extend current rates — it would also include some additional targeted tax relief. For starters, the bill would raise the $10,000 cap on the SALT deduction for state and local taxes to $30,000. And in many instances, taxes on tips, overtime and Social Security benefits would end.

Desirable as those measures are, they’ll dig Uncle Sam’s fiscal hole even deeper. What do congressional Republicans intend to do to compensate?

Well, they don’t want to jack up the top rate on incomes of $2.5 million or more from 37% to 39.6%. And they also don’t want to do away with the “carried interest loophole” used by private equity managers. Both of those ideas had Trump’s either tacit or explicit endorsement.

Instead, the bill’s architects decided to use the tax code to wage the culture wars — scrapping many tax breaks for electric vehicles and “clean” energy production, while looking to sharply raise the taxes paid by university endowments on their investment income.

But the real kicker to the bill is that it raises the debt ceiling by $4 trillion.

As a reminder, the debt ceiling has been in effect since Jan. 2 of this year. To stay under the $36.2 trillion ceiling, the Treasury has been resorting to “extraordinary measures” such borrowing against government pension funds.

“Including the debt ceiling in the broader bill will allow Republicans to avoid Democratic demands for concessions in exchange for their votes to raise the debt limit,” reports The Hill.

“But tacking debt limit action onto the same vehicle they’re using for Trump’s tax plans could also put a tight time crunch on Republicans to pass the sweeping tax bill.”

Indeed, Treasury Secretary Scott Bessent says his people will run out of accounting tricks by August — which means Congress needs to do something before its August recess.

Right now, that seems like a tall order: Blue-state Republicans are likely to hold out for a bigger cap to the SALT deduction. Deficit hawks, meanwhile, want far deeper spending cuts than anything currently on the table.

Recall that the Republican majority in the House is razor-thin. And while Speaker Mike Johnson has exercised an iron discipline over his fractious caucus so far, the legislation will be his biggest challenge yet.

If he can’t pull it off… and if the U.S. government actively defaults on the national debt…

Well, that’s why the bond market is freaking out anew. Stay tuned…

![]() Inflation: As Good as It Gets

Inflation: As Good as It Gets

The official inflation numbers are the tamest in over four years.

The Labor Department is out with the April consumer price index. It registered a 0.2% month-over-month increase, which works out to a year-over-year inflation rate of 2.3%. That’s the lowest since inflation started taking off in earnest in March 2021 (peaking over 9% in June 2022).

As always, these numbers likely bear no resemblance to your own cost of living.

It helped that energy prices fell 3.7% compared with a year earlier. But you were in a world of hurt last month if you needed your car fixed (up 5.6% year-over-year) or your auto insurance came due (up 6.4%) or you went to a ballgame or other sporting event (up 9.3%).

This month’s numbers are probably as good as it gets. As we’ve chronicled for a while now, once inflation sails past 5%, it typically takes a decade to get back to “normal” 2% levels.

Whether it’s the inflation numbers or something else, Wall Street is adding to yesterday’s big gains driven by the trade-war truce.

At last check the S&P 500 is up nearly 0.9% and only four points away from 5,900. The Nasdaq is up 1.5% and back above 19,000 for the first time since late February. The Dow is slightly in the red.

Precious metals are catching their breath after yesterday’s beat-down, gold at $3,247 and silver at $32.88. (Silver is quietly outperforming gold in recent days. Hmmm…) Crude is up big again, over 2.2% to $63.33, the highest in over two weeks.

Bitcoin is hanging tough at $103,642.

If small-business owners were worried last month about tariffs, you wouldn’t know it from the go-to source of small-business sentiment data.

The National Federation of Independent Business is out with its monthly Optimism Index, the result of a survey conducted during April.

The headline number fell 1.6 points to 95.8, the weakest since Donald Trump’s election last fall.

But contrary to what you might expect, uncertainty among survey respondents eased relative to previous months; the uncertainty index in April was no worse than it was last August.

As for the part of the survey where business owners are asked to identify their single most important problem, it seems good help is still hard to find — “quality of labor” was cited by 19%.

But for the first time in what seems like forever, inflation does not rank in the top two on this portion of the survey. Taxes are in second place, cited by 16%, followed by inflation at 14%. “Cost/availability of insurance” is creeping higher, now cited by 10%.

![]() Comic Relief

Comic Relief

![]() Readers Stand up for Tax Incentives

Readers Stand up for Tax Incentives

Because you never know what might get readers’ dander up… we were a bit surprised at the pushback to Saturday’s edition hitting out at the tax incentives for a new Microsoft data center in northwest Indiana.

“I always appreciate your contributions, but Saturday’s headline flashed red because La Porte is very nearby and I know and work with the consultants responsible for the transaction described in your article. And as a business/real estate transactional attorney, I’m involved in data center transactions for sellers, buyers and developers.

“I’m not suggesting that you shouldn’t provide a sensational headline to garner eyes, but would suggest that your article is missing several key components when looking at the larger landscape. One notable factor is that data center companies are not at all enthralled and trying to push back on the power supply regimen being adopted by Northern Indiana Public Service Co. — under which the power-generating stations for data centers will be separately funded by the data center users, which will pay commercial rates negotiated by NIPSCO on a user-by-user basis.

“And while I don’t know all of the specific detail of the public financing component, I did see some early outline of the underlying structure and understand how it will benefit the community, particularly since this data center will be developed upon land that would have nowhere near the tax-generating revenue this project would provide.

“In any event, this is good public discourse, but would suggest terms such as ‘scam’ and ‘holding the bag’ and portraying individuals I happen to know and respect as ‘tripping over themselves to hand out incentives’ are off the mark. That said, I’m not in your business, just a person looking to rely upon and benefit from the collective intelligence and experience of the Paradigm Group to make good decisions.”

Another reader was less kind and pushed back with what looks like the help of an AI engine.

“It literally took me 15 seconds to find out facts, and I already knew about the huge advantages to a community when the city government negotiates a large tax credit.

Allowing a 30% tax credit for new businesses and industries can have several positive financial effects on a city government:

Increased Economic Activity: New businesses can boost local spending, leading to higher sales tax revenues.

Job Creation: More businesses typically mean more jobs, reducing unemployment and increasing income tax collections (if applicable).

Property Value Growth: New industries can raise property values, leading to higher property tax revenues.

Long-Term Tax Base Expansion: While initial tax credits reduce revenue, the growth in businesses and population can significantly expand the tax base over time.

Attracting Complementary Businesses: New industries often attract suppliers and related businesses, further boosting economic growth.

These benefits can outweigh the short-term revenue losses from the tax credits if the strategy successfully stimulates sustained economic development.’

“This has been going on for decades! And it’s turned around and launched numerous cities into their next generation of prosperity!

“Atlanta did it with the film Industry!

“La Porte is a tiny depressed town. This will rocket their city into a prosperous future!

“You people are idiots!”

Dave responds: Because it’s “idiotic” to think government has no place picking winners and losers?

As it happens, a boutique think tank called Good Jobs First is out with a report calling out state governments for being too eager to hand special favors to data center developers. From the executive summary…

At least 10 states already lose more than $100 million per year in tax revenue to data centers, the cloud-computing warehouses that were proliferating before artificial intelligence greatly accelerated their growth.

The industry’s high-velocity growth, combined with the virtually automatic structure of the state tax exemptions, is preventing states from making accurate cost projections. For example, in the space of just 23 months, Texas revised its FY 2025 cost projection from $130 million to $1 billion. Virginia, Texas and Illinois have each recorded revenue-loss spikes of more than 1,000% in recent years.

The loss of state spending control is surely worse than we can yet document. That’s because of the 32 states with tax incentives to data centers, 12 fail to disclose even aggregate revenue losses, much less company-specific subsidies as is common in economic development. Those 12 “dark” states include Indiana, North Carolina and Utah, all of which have substantial and/or growing data center investments.

Don’t get us wrong. The lower corporate taxes are, the better. But those low rates should apply to everyone; trouble snowballs whenever government starts playing favorites.

Best regards,

Dave Gonigam

Managing editor, Paradigm Pressroom's 5 Bullets

")

")

")

")

")

")

")

")

")

")