SpaceX: There Is No Choice

![]() SpaceX: There Is No Choice

SpaceX: There Is No Choice

We’ve spent days if not weeks trying to warn you off buying SpaceX shares on IPO day.

We’ve spent days if not weeks trying to warn you off buying SpaceX shares on IPO day.

Which… in case you just emerged from a no-internet retreat in the Himalayas or something… is tomorrow.

History just isn’t on your side. We’ve cited the case of Facebook — down 54% in its first 12 months after going public in 2012.

Similar sob stories took place with Twitter (down 60%) and Robinhood (down 80%).

Yes, they all roared back to trade at many multiples of their IPO price — but, really, how many people had the patience to hold on?

All that said — and we realize we’re about to invoke one of the most dangerous phrases in all of investing — this time might be different.

To illustrate why, colleague Davis Wilson of our sister e-letter The Million Mission offers this analogy: Your spouse sends you to the grocery store with a shopping list from which you’re not to deviate one iota.

The list includes Honeycrisp apples — which turn out to be $450 a pound.

You buy Honeycrisp apples, the insane price be damned. There is no choice. The list is the list.

“Believe it or not, this is exactly how trillions of dollars are invested every day,” says Davis — “without the slightest thought given to the price paid.

“The shoppers are index funds — like QQQ, SPY, VOO, etc.

“The shopping list is a list of stocks that are chosen by the men and women working at Nasdaq, MSCI and Standard & Poor’s.

“And thanks to recent rule changes at Nasdaq and MSCI, SpaceX could find itself on some very important shopping lists shortly after its IPO.”

As you likely know, an index fund doesn’t try to beat the market. It tries to reflect its underlying index as closely as possible.

“If the index owns Nvidia, the index fund owns Nvidia,” says Davis. “If the index owns Microsoft, the index fund owns Microsoft. And if the index adds SpaceX, the index fund must buy SpaceX.”

If the fund manager thinks SpaceX is too pricey, too bad — he has no choice. The list is the list.

“Hisotorically,” says Davis, “newly public companies had to wait months or even years before being added to major indexes. That delay gave the market time to absorb the new shares and establish a fair price.”

Not so with SpaceX — not with expectations the company will raise $75 billion at a valuation over $1.75 trillion.

“Nasdaq recently changed its rules to allow certain mega-cap IPOs to enter the Nasdaq-100 after just 15 trading days,” says Davis.

“The Nasdaq-100 has roughly $1.4 trillion benchmarked against it through ETFs, mutual funds, retirement accounts and institutional portfolios.

“If SpaceX entered the index with a 0.5% weighting — which it’s expected to — those funds would need to buy roughly $6 billion worth of shares. At a 1% weighting, the figure rises to $12 billion.”

And then there’s MSCI — which has a similar fast track that could add qualifying companies in as little as 10 trading days.

“Approximately $5.8 trillion is benchmarked to MSCI indexes globally,” says Davis. “Even a relatively small weighting could translate into another $10 billion or more of buying demand.

“Add everything together and it's not difficult to envision $20–30 billion of ‘forced buying’ arriving within weeks of the IPO,” Davis says.

“And that's before hedge funds get involved… active managers decide they need exposure… financial advisers recommend the stock to clients… and retail investors like us pile in.

“Think about that for a second.

“SpaceX may raise $75 billion in the IPO. Then, just days later, tens of billions of dollars of additional demand could arrive from investors who are required to buy the stock at any price.”

In that atmosphere, valuation won’t matter. The index fund managers must buy. There is no choice. The list is the list.

![]() Dot-Com Echoes? Yes, But…

Dot-Com Echoes? Yes, But…

For all the stock market’s choppy action in the last week, history suggests the bull market isn’t over yet.

“Over the past several weeks,” says Paradigm trading pro Enrique Abeyta, “I have seen dozens of rare technical signals that all point to the same thing: The stock market will be HIGHER in one year.

“There have only been a few times in my 30 years as a professional investor when I have had this degree of confidence that the stock market will be higher in a year.

“The last time was after the COVID shutdowns, when I (correctly) predicted that we would see one of the greatest periods of GDP growth since World War II.”

For sure, Enrique sees parallels between the AI boom now and the dot-com boom of the late 1990s. But as he’s said for several months, there’s no indication we’re at a “March 2000 moment” — when the Nasdaq began a sickening 78% slide.

At worst, he says we’re at a June 1999 moment — in which case the Nasdaq was still up 61% a year later, a period including the first three months of the big sell-off!

If you’re looking for indications when “the top is in,” Enrique says watch the Federal Reserve.

Here’s a chart of the fed funds target rate over the course of his career. Note the red arrows when the Fed was raising rates.

In each case, those rate-raising cycles preceded the onset of a bear market.

True, the precise interval between the start of the rate-raising cycle and the start of the bear market varies. But the point now is that the Fed has not yet begun a new rate-raising cycle.

As such, the bull still has room to run.

After a tough day yesterday, the major U.S. indexes are staging a modest recovery.

The S&P 500 is up 0.6% at last check, back over 7,300. The Nasdaq and the Dow are both up well over three-quarters of a percent.

Gold has clambered its way back over $4,100. Silver’s back above $64. But Bitcoin is still mired below $63,000 and Ethereum in the $1,600s.

The big economic number today is wholesale inflation — and it’s scary-bad, up 1.1% month-over-month and 6.5% year-over-year. It’s the biggest increase since November 2022.

These increases feed through to the consumer with a lag — at least two months, sometimes much longer.

And you can’t blame it all on the war driving up fuel prices. If you throw out food and energy, the year-over-year increase is still a blistering 4.9%. That means the primary culprit is a federal government that still can’t get deficit spending under control.

![]() Inflation and War

Inflation and War

“I love the inflation,” said Donald Trump yesterday in a remark that predictably went viral.

He was in the Oval Office, asked by reporters about the consumer-level inflation numbers that had just come out. At 4.2%, the official inflation rate is the highest in three years.

To be sure, those four words standing alone need context. Unfortunately, the context the president provided was an incoherent jumble — a word salad in which he seemed to suggest that people will be happy once the inflation rate starts coming back down. (If you wish, you can parse it yourself. Good luck.)

Which is more or less what Buck Sexton, syndicated radio host and editor of Paradigm’s Money & Power, thinks the president is betting on.

With midterm elections less than five months away, it’s all about perceptions — as he told his subscribers last Friday: “Let's say tomorrow morning, investors wake up and become convinced that the Strait of Hormuz is staying open and that the worst of this is behind us. Oil prices would probably start reacting before a single thing actually changes on the ground.

“Trump doesn't need perfection here. He needs people to feel like things are getting better. That's it.

“The faster the White House can convince people that prices are headed in the right direction, the better everybody's life gets — including Republicans running for reelection this year.”

In the meantime, though, even The Babylon Bee — the conservative parody site — is posting headlines like this.

True, it doesn’t lay blame for the war at Trump’s feet. But still…

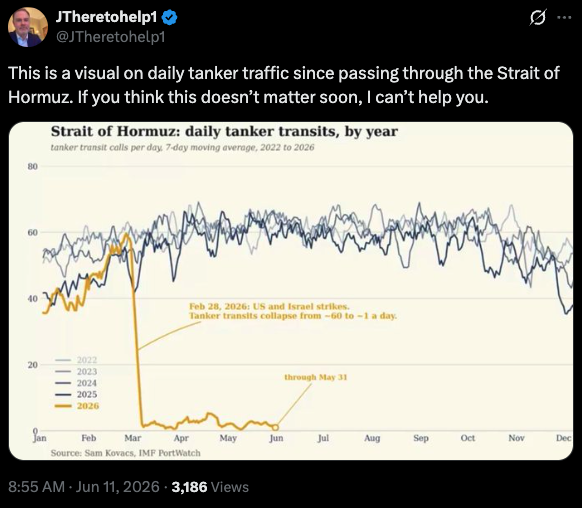

Oil traders are writing off Trump’s latest threats to attack Iran “VERY HARD TONIGHT.” As we write, U.S. crude futures are up only 1.5% to $91.38.

For the first time since April, the president is suggesting U.S. forces will try to seize Iran’s big oil terminal at Kharg Island — an undertaking that’s no less fraught with peril now than it was then.

The latest shooting between the U.S. and Iranian sides began in earnest late Sunday/early Monday when a U.S. Apache helicopter was downed over the Strait of Hormuz.

The incident remains murky more than 72 hours later. Tehran hasn’t claimed credit for bringing the copter down. Axios reports that Washington still hasn’t determined whether the Iranians brought it down on purpose. (Yeah, I know, Axios. Still…)

The anonymous military blogger known as “Big Serge” poured cold water on Trump’s account of what happened: “Love the idea of a drone with the precision to spear the cockpit of a moving helicopter and then catch fire like a cheap toaster instead of exploding.”

In any event, Washington says the pilots were rescued. And the Strait of Hormuz remains all but closed.

![]() Comic Relief: America, RIP?

Comic Relief: America, RIP?

So… this is an item available at Walmart — 100 for $2.97…

Yeah, I know, it commemorates the nation’s 250th birthday.

But it also looks… like… a headstone?

Does someone know something?

![]() Mailbag: More Property Taxes

Mailbag: More Property Taxes

In an unexpected development, our reader-mail thread in recent days about a property tax referendum in Florida has prompted a flurry of feedback from… California.

“As ominous as it may sound,” says one reader, “California did one thing right back in the 1970s — they passed Proposition 13.

“It limits property taxes to 1% of the purchase price of the property, with a max 2% annual increase. As a result, long-term property owners enjoy a reasonable tax burden in retirement.”

“All this talk about the Florida property tax initiative reminds me of my parents dragging me to a stuffy, high school cafeteria to hear some guy named Howard Jarvis talk about Proposition 13, which was going to cut property taxes and restore the American dream,” writes another.

“And I remember how, over the next few years, those in charge of local governments and school districts made the most painful, most public cuts possible to punish the ignorant electorate for threatening their gravy train.

“Ah the memories.”

“Proposition 13 is a subject of hot debate every election cycle,” says a third.

“Reading all of the feedback you've published, along with what I'm hearing out here, it's all the same and your last paragraph on Tuesday summed it up perfectly.

“The real question isn't how to shift the tax burden. The part that rarely gets brought up, but is the most important question, is what ought the government be funding in the first place. In my opinion, the answer is a helluva lot less than it currently does. The list of things my taxes fund which I find repugnant is too long to include here, and I imagine that's true for most people.

“Perhaps if we'd get back to only funding actual essential services, we could figure out how to fund them without so much vitriol. Of course, that requires someone deciding for us all what is and isn't 'essential,' and those decisions are almost always made with influence from the beneficiaries/providers of said services.

“It looks like we may actually avoid empirical collapse for another generation. While that is in many ways a relief, it is also somewhat of a disappointment. A clean slate would have been another chance to get it right.

“The path we're on, which is likely to preserve the U.S.' status as the issuer of the world’s reserve currency for a while longer, will certainly come with more central planning and control of the economy. Financed on the backs of the citizenry, with made-up dollars. Taxes aren't going away; the only question is how we choose to arrange the deck chairs while the band plays on.

“You're not the only one who gets accused of cynicism BTW.”

Dave responds: Heh.

I’ll leave the dying-empire discussion for another time and keep the focus on California. The first reader’s comment about “a reasonable tax burden in retirement” comes with a caveat, one I’ve spotlighted before.

If a longtime California homeowner wants to downsize to a locale with low (Arizona) or no (Texas) state income taxes… he or she will take an enormous one-time hit with federal income taxes.

Under the Taxpayer Relief Act of 1997, there’s an exemption on any capital gains you rake in from the sale of a personal residence — $250,000 for individuals, $500,000 for couples.

Even though this legislation was passed more than a generation ago, those thresholds have never been adjusted for inflation. If they were, they’d be $515,000 for individuals and $1.03 million for couples.

And even those higher figures wouldn’t be fair — considering that home prices have risen much faster than the inflation rate.

It hits hard everywhere — but especially in California where pretty much anyone with a paid-off house is a “millionaire.”

Come to think of it… You hear a lot of complaints these days about why the boomers won’t downsize, which has the effect of shutting younger people out of homes that can accommodate growing families.

There are many reasons behind the phenomenon, no doubt — but the silly-low federal capital gains exemption has to be a big one…

")

")