13 Banks on the Brink

![]() Big Banks Bury CRE Losses

Big Banks Bury CRE Losses

“Recall the banking crisis of March 2023,” says Paradigm’s macro expert Jim Rickards.

“Recall the banking crisis of March 2023,” says Paradigm’s macro expert Jim Rickards.

“It began with the collapse of the little-known Silvergate Bank on March 8, followed the next day by the collapse of the much larger Silicon Valley Bank (SVB).

“SVB had over $120 billion in uninsured deposits. (Bank deposits over $250,000 each are not covered by FDIC insurance.) Those depositors stood to lose all their money over the insured amount.

“This would have led to the collapse of hundreds of tech start-ups in Silicon Valley who had placed their working capital on deposit at SVB,” Jim says.

“There were also larger businesses such as Cisco and at least one large cryptocurrency exchange that had billions of dollars deposited at SVB. Those businesses would have taken huge write-downs based on the size of their uninsured deposits…

- “On March 9, the FDIC said that excess deposits were uninsured, and depositors would get ‘receivership certificates’ of uncertain value and zero liquidity instead

- “By March 11, the FDIC reversed course and said all deposits would be insured,” Jim says.

“The Federal Reserve intervened and said they would take any U.S. Treasury securities from member banks in exchange for par value in cash, even if the bonds were only worth 80% of par (which most were).

“That Sunday night, March 12, they also closed Signature Bank, a New York-based bank with crypto links.

“The damage wasn’t done: Credit Suisse was on the edge of insolvency. On March 19, the Swiss National Bank forced a merger of UBS and Credit Suisse, one of the largest banks in the world.

“Finally, on May 1, First Republic Bank, with over $225 billion in assets, was closed by the government and sold to JPMorgan.

“After five bank failures in two months and a trillion-dollar bailout by the government, the crisis seemed over. But that was false comfort…

“At the time, I mentioned it was only ‘halftime.’ The second stage of the crisis would erupt in even more dramatic fashion sooner or later,” Jim asserts.

“My analysis was based on ‘quiet periods’ in the middle of the 1997–1998 Asia-Russia financial crisis,” he says, “and the 2007–2009 global financial crisis.

“Now it seems that the quiet period is over. We are entering stage two of the banking meltdown…

“New York Community Bancorp (NYCB) took huge losses of over $2 billion in February 2024 on its commercial real estate (CRE) portfolio. It has been teetering on the brink ever since.”

And despite Fed chair Jerome Powell claiming a looming CRE crisis is “a manageable problem” among “larger banks”... NYCB isn’t the only larger bank on the brink.

(Keep in mind, there are only 13 U.S. banks that meet the larger criteria.)

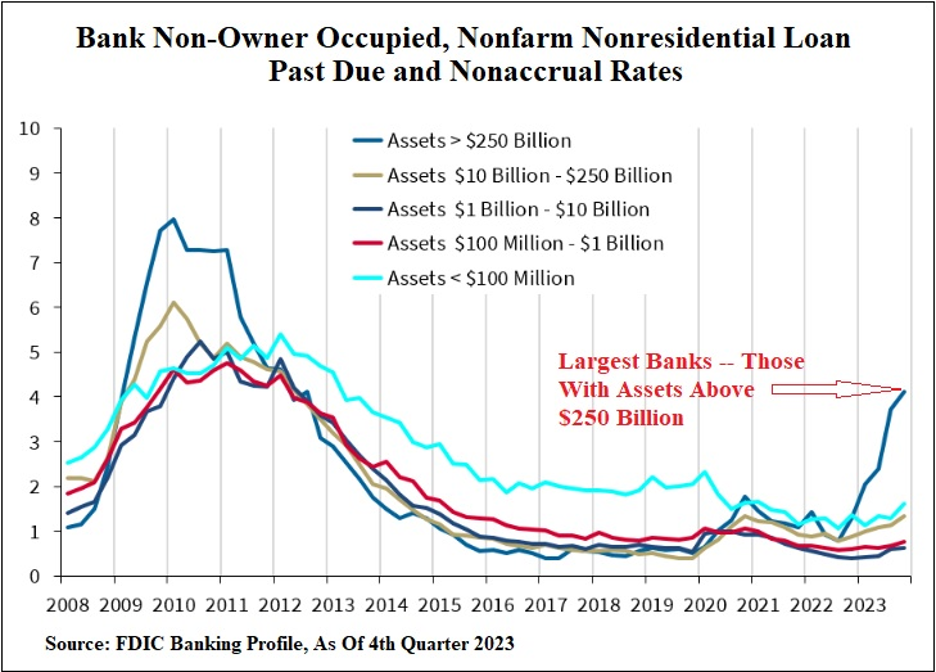

“In fact, [past] due loans on commercial real estate at the largest banks (those with more than $250 billion in assets) as of Dec. 31, 2023 are at 4.11%,” say Pam and Russ Martens at Wall Street On Parade.

Which, pfft, might not seem like a lot, but…

“That’s 1.66% higher than at the end of the fourth quarter of 2008 when banks were exploding all over Wall Street during the financial crisis,” the Martenses note.

“As the chart above indicates, commercial real estate problems quickly became a lot worse at the largest banks, with the past due rate reaching 7.97% by the end of the first quarter of 2010.”

[This is curious: The reason the most recent available data is from December 2023 is because the Fed stopped publishing data on loan losses at commercial banks — something they’d published quarterly since 1984… Yikes.]

Back to Jim: “On March 6, NYCB was bailed out with $1 billion of new capital raised by former Treasury Secretary Steven Mnuchin and Ken Griffin’s Citadel hedge fund,” he says.

“NYCB may have been bailed out, but it’s the canary in the coal mine…

“Its failure means that billions more in CRE losses are buried on bank books all over the country,” he adds.

“Stage two of the crisis is here,” Jim concludes, “and the effects will be devastating to financial institutions and the stock market as a whole.”

[You’re eligible to claim what Jim Rickards calls the most dangerous book in America…

“I’m urging everyone I know to read it within the next 30 days,” Jim emphasizes.

But with fewer than 500 copies left, we may run out of stock soon.

So here’s how to claim your copy:

- Watch Jim's short message

- Review your account information

- Confirm you’d like to accept Jim’s offer.

Remember, we have fewer than 500 in stock. Jim explains what you need to do to claim your copy.]

![]() Gold and Great Budget Deficits

Gold and Great Budget Deficits

Here’s an upside-down reality today: “[You’ve] probably noticed that rates and gold are now positively correlated. Why?” X-tweets author Jared Dillian (aka @dailydirtnap).

Or as another X-tweet contextualizes (with gold’s price chart)...

➢ “Gold responds to a number of different economic variables, but the one that it has the highest correlation to is budget deficits,” he says. “When deficits are large (like 2009–2011), gold goes up,” Dillians says. “When deficits are small (like 2011–2016), gold goes down.”

Fast forward to Nov. 5, 2024: Invariably, the next president — whomever it is — will have a monstrous budget deficit on his hands. Got gold?

Gold and silver are both catching bids again today — to a record high $2,347.80 per ounce for gold and just under $28 for silver. Crude, however, has pulled back over 1% to $85.94 for a barrel of West Texas Intermediate.

Switching gears to stocks, the Dow and S&P 500 are slightly in the red at 38,900 and 5,200 respectively. Holding onto green for dear life, the tech-heavy Nasdaq is up to 16,255.

The crypto market is in recovery mode. Bitcoin is up 3.75%, just under $72,000, while Ethereum is up, wow, almost 8% to $3,600.

![]() The IRS Has a Labor Shortage

The IRS Has a Labor Shortage

“President Biden's plan to hire a new army of tax collectors is falling flat, and the agents already at work are targeting the middle class,” The Wall Street Journal reports.

As part of the so-called Inflation Reduction Act of 2022, the IRS received an $80 billion cash infusion to, in part, hire some 87,000 new IRS agents — some of whom would actually be armed (and dangerous?).

Who could have predicted that, instead of targeting lawyered-up millionaires and billionaires as Biden and Yellen promised, the IRS would turn on everyday Americans? Oh, nevermind. We did…

In September 2023, for instance, we asked: “You never really believed the IRS was going to limit its stepped-up enforcement efforts to people with incomes over $400,000, right?”

Now, the WSJ has the receipts:

- “As of last summer, 63% of new audits targeted taxpayers with income of less than $200,000

- While 80% of audits covered filers earning less than $1 million.”

And this is embarrassing: Instead of beefing up the number of IRS agents, goon squad staffing actually shrunk 8% during 2019 – March 2023.

According to industry publication Government Executive: “IRS had planned to bring on 3,833 revenue agents in fiscal 2023, but in the first six months officials had recruited just 34.”

We repeat: Thirty. Four.

Despite “eclipse-pocalypse,” Monday just got a little brighter…

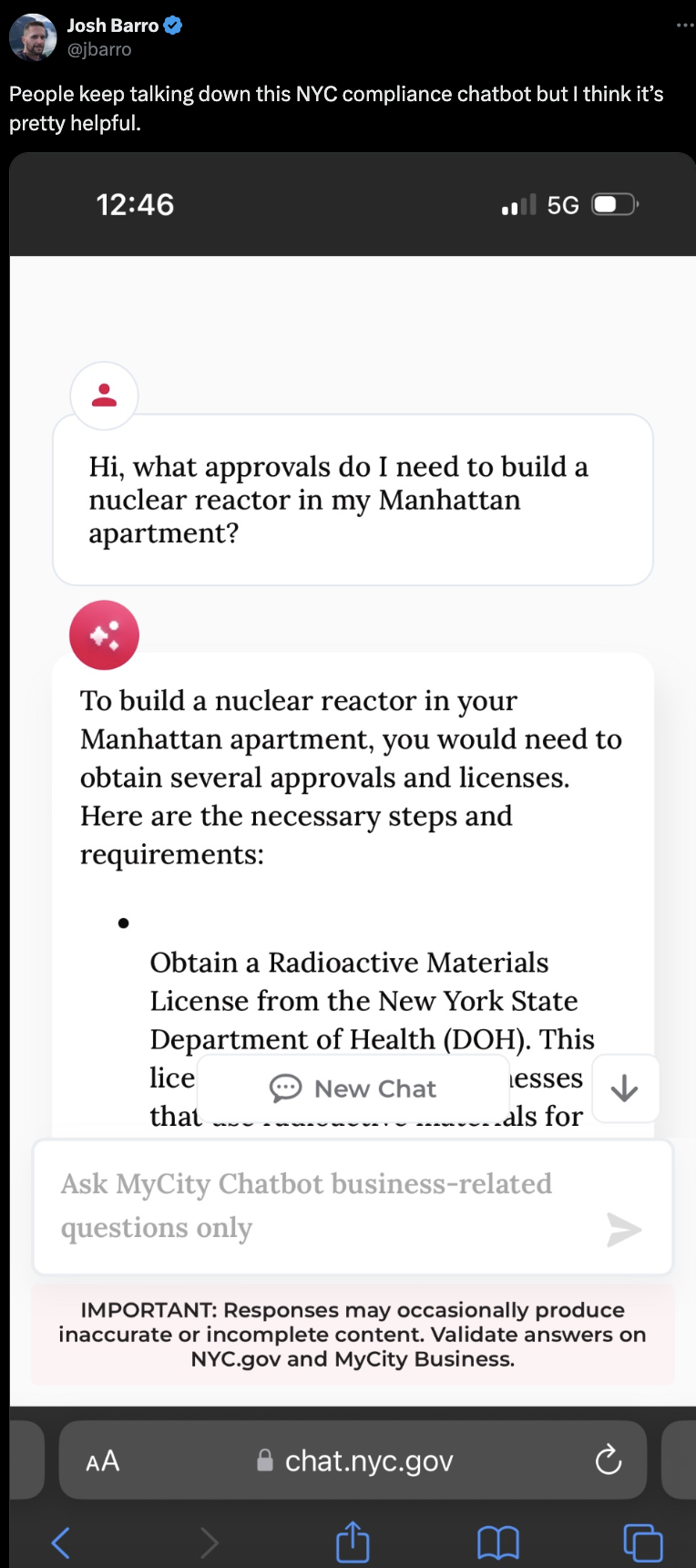

![]() An AI Fiasco in NYC

An AI Fiasco in NYC

New York City Mayor Eric Adams defends a blinkered AI-powered chatbot meant to help local business owners. “You need to put it into the real environment to iron out the kinks,” Adams exclaims.

“In October, the MyCity chatbot was touted as the first citywide use of such AI technology, something that would give business owners ‘actionable and trusted information’ in response to queries typed into an online portal,” Reuters notes.

Et voila…

Among the more disgusting advice the chatbot has proffered? It’s given the OK to a deli for serving cheese — nibbled by rats! — to customers.

“The chatbot [relies] on Microsoft's Azure AI service,” Reuters adds. “Microsoft declined to say what might be causing the problems, but said in a statement it was working with the city to fix them.”

Regardless, the chatbot is up-and-running today. Presumably, still working out “the kinks.”

![]() Mailbag: YOLO, Vegas and NYC’s Scaffolding

Mailbag: YOLO, Vegas and NYC’s Scaffolding

“If YOLO is your approach to investing, go to Vegas for better odds,” a reader writes, answering Friday’s question: Why do you have money in the markets?

“I agree ‘you only live once,’ but I would like to think that I'm gonna live for a good long while. I'm in the Altucher's Investment Network because I want to live that good long time without having to keep working for someone else until I can't physically work anymore.

“As far as memecoins, if you decide to produce a premium trading service for memecoins, I will not be signing up. I wouldn't sign up for it even if it was a free add-on to what I currently have because memecoins, like leaves, look good for a season and then drop. No thank you.

“I'm more of an ‘invest and forget about it’ kind of guy.”

“YOLO, yes, it’s true,” says another contributor. “Tomorrow is not promised, but…

“I invest money in the market today with the hope of living better in the future. Like a seed, money must be taken care of in order to grow. I RISK and invest today so that my progeny will have more fruitful lives in the future.”

Last, two readers comment on the yawning disconnect between the so-called “economy” and the lived experience of everyday Americans.

“Since you’re on the topic of New York, consider the Local Law 11 grift,” a reader writes after reading Saturday’s missive about buggered legal marijuana in the Empire State.

“This law on building facade safety could be well-intentioned, but it results in inspections and repairs of buildings every five years.

“It is not only littering NYC with scaffolds, but costing co-op and condo owners over $1 million per building every five years. It’s making local contractors, engineers and architects rich by squeezing middle class New Yorkers.”

Then there’s this peek behind the first-class curtain…

“Decades ago when 401(k)s were being rolled out and corporations needed more buy-in from us low-level employees (so C-suite employees could participate at higher levels) the corporate rep included in his presentation an annual wage increase of 5% to show us how our money could grow into the millions.

“Well, he found out very quickly that we did not get annual increases (usually, every other year) and that our raises were about 2.5%.

“We thanked him, however, for revealing what our bosses got!”

Too funny.

We’ll be back tomorrow with another round of 5 Bullets. Take care!

Best regards,

Emily Clancy

Associate editor, Paradigm Pressroom's 5 Bullets

")

")