Main Character Monetary Policy

![]() Fed Fallout: Main Character Energy

Fed Fallout: Main Character Energy

“This is how monetary policy is made in emerging markets with weak institutions.”

“This is how monetary policy is made in emerging markets with weak institutions.”

That sentence appeared in a joint public statement released this month by former Federal Reserve chairs — including Janet Yellen, Ben Bernanke and Alan Greenspan — responding to the Justice Department opening a criminal inquiry into Fed Chair Jerome Powell.

Such tactics, they say high-handedly, have “highly negative consequences for inflation and the functioning of [economies] more broadly… It has no place in the United States, whose greatest strength is the rule of law, which is at the foundation of our economic success.”

Days later, President Trump told the World Economic Forum in Davos: “I’ll be announcing a new Fed chairman in the not too distant future,” adding “we have a terrible chairman right now.”

The reaction from the Davos set was swift — and anxious. Which is understandable. But it also invites a reality check.

Federal Reserve independence has never been absolute. Presidents have pressured central bankers for as long as the institution has existed.

In the 1960s, for instance, President Lyndon B. Johnson physically manhandled Fed chair William McChesney Martin over interest rates.

Martin’s successor, Arthur Burns, accommodated President Richard Nixon ahead of the 1972 election, a decision that helped fuel the inflationary mess of the 1970s.

More recently, President Joe Biden publicly reminded Powell that getting inflation under control rested squarely on the Fed.

“To this day the 12 regional Federal Reserve banks are owned privately by the banks in each region,” Jim Rickards notes. “Direction is provided by the Board of Governors of the Federal Reserve System appointed by the U.S. president and based in Washington, D.C.

“The overall system is a perfect hybrid of public and private interests.”

So the idea that Trump has shattered some previously pristine norm is overstated. What has changed is the scale of the Fed’s power — and the consequences of wielding it so openly.

After the 2008 financial crisis, the Fed and its global peers crossed lines that once seemed uncrossable.

Policy rates fell to zero or below. Quantitative easing (QE) expanded central-bank balance sheets by trillions. The European Central Bank, the Swiss National Bank and the Bank of Japan all followed similar paths.

Markets responded exactly as intended. Asset prices soared, borrowing costs collapsed and governments discovered they could finance deficits cheaply and almost indefinitely .

The lesson for elected officials was unavoidable: Monetary policy could stimulate the economy faster and more forcefully than fiscal policy ever could.

As Eric Salzman writes at Racket News, that lesson dramatically increased the temptation to influence the Fed:

By deploying extraordinary monetary policy from 2008–2018 and then from 2020–2022, the Fed has shown every president, both present and future, that those powers can juice the economy in ways that fiscal policy can rarely match.

Once a central bank demonstrates it can move markets with a sentence, presidents inevitably care who holds the microphone at post-FOMC press conferences.

That microphone amplified under Alan Greenspan — nickname: “the Maestro” — whose tenure marked the Fed’s brush with mainstream celebrity.

And it reached a fever pitch after the financial crisis of 2008 when Ben Bernanke rewrote the central-bank playbook with zero rates, massive asset purchases and a banking-system bailout — later memorialized in Bernanke’s self-aggrandizing memoir.

Bernanke’s book advance has never been disclosed…

Bernanke’s book advance has never been disclosed…

From that point forward, the Fed was no longer just a regulator. It had, to quote the kids, main character energy.

FOMC meetings became national events, press conferences were parsed like earnings calls and regional Fed presidents became media fixtures. They traveled to Davos and Jackson Hole not as technicians, but as global figures.

This visibility was not imposed on the Fed. It was chosen. And once chosen, independence became harder to defend. A central bank that cultivates such attention cannot plausibly claim insulation from politics.

That’s the missing context behind the Lisa Cook case.

When Trump moved to fire Fed governor Lisa Cook for cause — citing alleged mortgage fraud — Cook refused to leave, setting off a legal fight now before the Supreme Court.

This week, SCOTUS heard arguments in the case. The justices’ questions signaled real discomfort with the idea that a president could unilaterally declare “cause” under the Federal Reserve Act.

For now, Cook remains on the job while the courts sort it out. (It’s fair to note that no court has ruled that Cook committed mortgage fraud for two homes purchased in 2021.)

But the episode exposes the Fed’s real vulnerability. This is the price of prominence. A quieter Fed — one that operated without the aura of omnipotence — might be harder to target. (Perhaps Ms. Cook’s mortgage paperwork would not have drawn this level of attention?)

True, the Fed has never been truly independent from politics. Presidents have always leaned on, nudged and sometimes even shoved.

But what changed after 2008 is the Fed showed off how much it can do — indefinite QE, asset purchases, full-spectrum market support — and then built a public ritual around that power.

With power came attention. And power and attention invite attempts to control the institution — whether through nominations, investigations or court fights.

![]() Bond Exit, Stock Stampede

Bond Exit, Stock Stampede

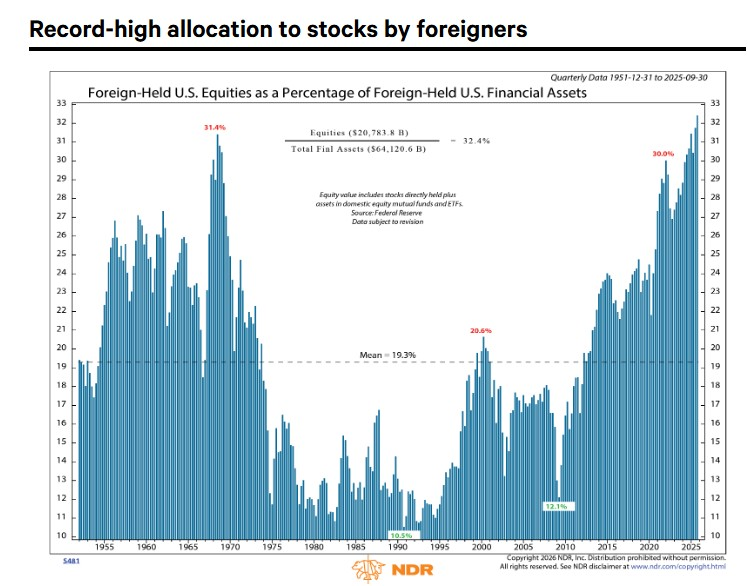

“While foreigners may be SELLING AMERICAN bonds, they appear to be BUYING AMERICAN stocks!” pro trader Enrique Abeyta emphasizes.

We touched on bonds earlier this week — using China as a clear example. Compared with January 2025, China’s Treasury exposure is now nearly 10% lower.

“Foreign-held U.S. equities as a percentage of foreign-held assets is at a new all-time high, breaking the previous record set back in 1968,” Enrique notes.

Source: NDR Inc.

Source: NDR Inc.

Stocks are setting up nicely this afternoon. The Nasdaq’s up 1% to 23,460 while the Dow and S&P 500 are up 0.80% and 0.65% respectively.

As for crude, it’s down 2%, under $60 for a barrel of WTI. But gold and silver are scorching hot! At record-breaking prices, in fact. Gold’s up 1.70% to $4,920 per ounce, and silver’s up 3.70% to $95.

The crypto market, however, is seeing red. Bitcoin’s down 0.40% to $89,500 while Ethereum’s down 2.45% to $2,945.

![]() The New Gold Order

The New Gold Order

For most of the modern era, gold pricing power rested firmly in the West.

“The world’s gold trade revolved around two cities: London and New York,” says Fiore Group CEO Frank Giustra. Those markets — anchored by the London Bullion Market Association and New York’s futures exchange (COMEX) — set prices for bullion across the globe.

Giustra’s career unfolded inside that system. In the 1980s, he moved to London to help finance junior mining companies, raising capital as European institutions piled into gold. The structure was clear and dollar-centric.

“The prices you see ticking across your screen today — ‘spot gold’ and ‘gold futures’ — still come from the London Bullion Market Association (LBMA) and COMEX,” he writes. Every ounce, regardless of origin, was priced in U.S. dollars.

That dominance was a legacy of Bretton Woods. In 1944, the dollar was pegged to gold at $35 an ounce, reflecting the United States’ postwar stockpile and economic strength. When President Richard Nixon closed the gold window in 1971, the system shifted to pure fiat.

As Giustra puts it, the message became: “Trust us — our economy’s strong, and our money’s as good as gold.” The petrodollar system, meanwhile, kept the dollar on top.

The first serious challenge emerged in 2002, when China launched the Shanghai Gold Exchange. It introduced something missing from Western markets: mandatory physical delivery.

While Giustra estimates around 95% of trades on COMEX are paper contracts, Shanghai required real bullion to change hands, at least domestically.

But China went further in 2014 with the Shanghai International Gold Exchange, allowing foreign participants to trade gold in yuan rather than dollars. In 2016, it introduced the Shanghai Gold Benchmark Price, a daily yuan-denominated auction. For the first time in a century, London had a serious counterpart.

Global events amplified the shift. The 2008 financial crisis exposed the fragility of leverage and monetary expansion. COVID-era stimulus accelerated it. Then, in 2022, the freezing of Russian reserves forced other nations to ask, as Giustra observes: “What if we’re next?” Central banks responded by buying physical gold and reducing reliance on dollar assets.

The result has been a slow rebalancing. “The Shanghai Gold Exchange won’t replace COMEX or LBMA overnight,” Giustra says, “and the dollar won’t vanish tomorrow.” Still, every trade settled in yuan and every bar vaulted outside Western control marks a subtle transfer of power.

Giustra is a long-time power broker in mining and metals; he’s been around these markets long enough to recognize structural change when he sees it. If gold is quietly reclaiming its role as real money, Shanghai — not London or New York — may be the future.

![]() “AI Tax” (Not What You Think)

“AI Tax” (Not What You Think)

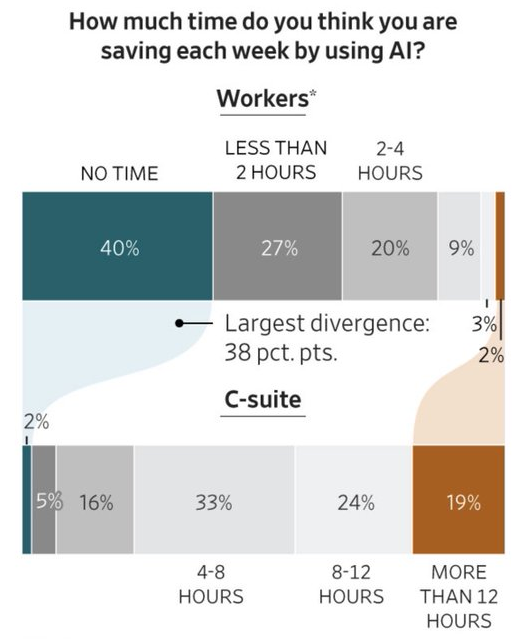

A study of 5,000 white-collar workers by the AI consulting firm Section finds a striking disconnect between executives and employees when using the AI tools.

Two-thirds of nonmanagement employees respond AI saves them less than two hours per week — or no time at all. More than 40% of executives, meanwhile, report saving over eight hours a week.

Source: Section, Stephanie Stamm, Wall Street Journal

Source: Section, Stephanie Stamm, Wall Street Journal

“Executives automatically assume AI is going to be the savior,” says Steve McGarvey, a user-experience designer in Raleigh, N.C. “I can’t count the number of times that I’ve sought a solution for a problem, asked an LLM and it gave me a solution [that] was completely wrong.”

McGarvey says AI helps with research — but only if you already know enough to spot when it’s wrong. “Unless you have some judgment or discernment in the field you’re in,” he adds, “you could really do harm.”

That friction has a cost. A report from Workday calls it an “AI tax” on productivity: time saved, then quietly spent correcting errors. Even at the top, the payoff remains elusive. In a PricewaterhouseCoopers survey presented at Davos, just 12% of CEOs say AI delivered both cost savings and revenue gains.

But some companies have already tested AI’s limits. And then re-tested. Klarna replaced hundreds of customer-service agents with AI — then rehired humans for harder questions. Duolingo said AI would replace contractors, then ended 2024 with a 14% larger staff.

Bottom line: Workers aren’t impressed. To wit, 40% of respondents say they’d be fine never using AI again.

[At the Paradigm app’s Daily Feed, our managing editor Dave Gonigam commented on this story: “Somewhere in the Great Beyond, Dilbert creator Scott Adams is having a hearty laugh.”

Haven’t downloaded the app yet? Join thousands of your fellow Paradigm subscribers at the instructions right here.]

![]() Trump 2.0

Trump 2.0

“Better off,” a longtime reader responds to Trump’s assessment. “Over the last three years, as octogenarians, we assiduously eliminated all debt, including the home equity loan.

“Then we sold municipals and converted to energy and miners with reinvested dividends. We are steadily adding to our net worth every month. We feel more secure now than we did one–three years ago. Guidance from Paradigm has been a great help.”

“I am financially worse off,” says another contributor. “As a retiree, the rising costs of food, Medicare and onerous taxes are hurting me.

“I am totally irritated that the Social Security miserly increases are completely wiped out just by the increases in Medicare costs. But the real kicker to me is the money in both Social Security and Medicare is MY money.

“I worked for 40 years, made over six figures and maxed out my 401(k) yearly. I should be living comfortably, but I have to pull from my retirement monthly just to stay in my home. We've given up eating out, vacations, concerts and theater.

“I understand how policies Trump is working to institute will help our country; it just may be too late for me.”

“Has the Trump 2.0 administration made me better off than I was a year ago?” adds our final correspondent today.

“Financially, yes. But only because his immigration policy has opened up thousands of jobs in

detention operations. A new detention facility opened up in my state, and I was able get a

job that pays 50% more under a federal contract than what I was making in the same position

working in a state-run prison. Not everyone is so fortunate.

“As for his economic policies, I agree that capping interest rates is a VERY BAD idea. The jury is

still out on all of his tariffs, and will be for some time. I remain optimistic that the long-term

gain will be worth the (hopefully) short-term pain.

“Of course, the above goes out the window if his foreign policy gets us all incinerated.”

Thanks to everyone who took the time to write in — the notes, stories and perspectives are genuinely appreciated.

More soon… And thanks for being part of the 5 Bullets family!

")

")

")

")

")

")

")

")