The Underground M&A of 2026

![]() The Biggest “Underground” M&A of 2026

The Biggest “Underground” M&A of 2026

There’s a scene that plays out at big industry trade shows that most people never hear about. The main floor is all noise and spectacle — gleaming displays, flashing lights, cocktail receptions.

There’s a scene that plays out at big industry trade shows that most people never hear about. The main floor is all noise and spectacle — gleaming displays, flashing lights, cocktail receptions.

But down the hallway, in a private suite with a closed door and two suits standing outside, that’s where the real business gets done. That’s where billions of dollars change hands.

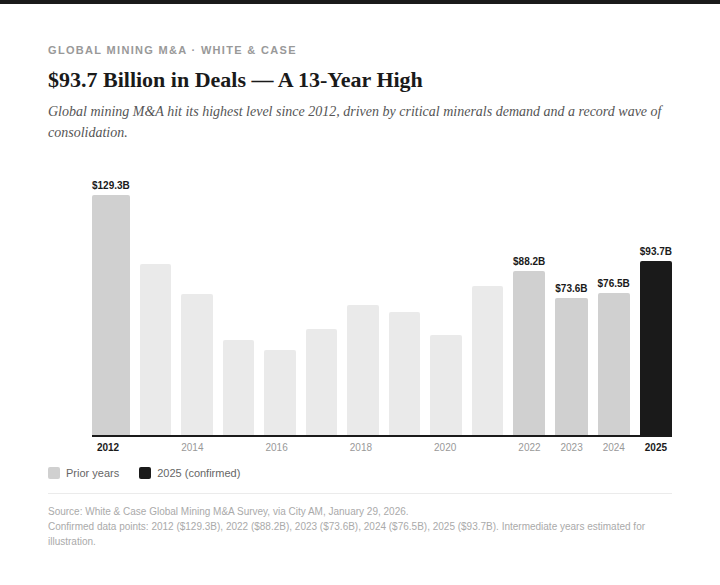

2025 was that kind of year for the global mining industry.

According to the law firm White & Case, the aggregate value of global mining M&A hit $93.7 billion last year — the highest annual total since 2012.

That wasn’t a fluke. It was the inevitable collision of three forces building for years:

- Surging demand for critical minerals

- A Washington policy environment determined to reduce dependence on foreign supply chains

- And over $1 trillion in private equity dry powder looking for a home.

The policy piece is the one most investors are still underestimating.

On Jan. 14, 2026, President Trump issued a presidential proclamation directing negotiations under Section 232 on critical minerals — invoking a national security authority typically reserved for steel and aluminum.

The official list of covered minerals — 50 in 2022; expanded to 60 in 2025 — includes zinc, gallium, germanium and dozens of others essential to defense, energy and technology.

The message to the market was hard to miss: Washington considers these materials a matter of national defense, not just industrial supply.

Rebecca Campbell, global head of mining and metals at White & Case, foreshadows: “In 2026, strategic partnerships between governments, government agencies and the private sector are likely to be the backbone of growth M&A in the sector.”

Translation: The deals getting done this year won’t just be driven by commodity prices. They'll be driven by geopolitics.

China, in particular, currently acts as the world's predominant critical minerals refiner — and has already weaponized that position by restricting exports of gallium and germanium in recent years.

For mining companies sitting on domestic deposits of these materials, that geopolitical pressure is doing something remarkable: It's making them acquisition targets almost by default.

For a major mining conglomerate that needs these minerals and can't reliably source them from China, buying an American producer outright is faster, cheaper and safer than building a new mine from scratch.

Bain & Co., the global management consultancy that tracks dealmaking across every major industry, captures the mood: “The next wave of dealmaking will be bigger, more complex and far more decisive in determining who wins the forthcoming super cycle.”

Global M&A across all sectors surged to near-record levels in 2025, with megadeals above $5 billion accounting for the lion’s share of value growth.

Which tells you something important: In a buyout boom, the big money doesn’t get spread around evenly. It concentrates. And the investors who captured it weren't the ones who owned a little of everything — they were the ones already holding shares of the right target when the announcement hit.

But targeted companies don’t announce it in advance. Deals are assembled quietly, in private suites, on encrypted calls between lawyers.

By the time a buyout hits the wire, the easy money is already made. Unless, of course, you know what to look for before the announcement.

[Editorial Note: Chinese smelters are warning that escalating tensions in the Middle East could disrupt global supplies of a key rare mineral.

Iran ranks among the world’s top 15 producers — and Seatrade Maritime News reports the Strait of Hormuz is now “effectively closed to almost all international commercial shipping.”

If trade flows remain constrained, availability of this mineral could tighten suddenly.

That matters here at home. President Trump recently invoked Section 232 authority, designating this mineral as “critical to national security.”

In the U.S., a single mine accounts for roughly 70% of domestic production. Even before developments in Iran, James Altucher’s proprietary models outlined a scenario where shares of the company involved could deliver gains as high as 925% in the months ahead.

Given the potential for supply disruption, James and his team have updated their projections. Under certain conditions, his analysis now indicates upside that could reach as much as 2,464%.

Of course, outcomes depend on how events unfold. But if a supply shock takes shape, the opportunity may not remain overlooked for long.

You can review the full details here.]

![]() The 60/20/20 Portfolio

The 60/20/20 Portfolio

Per market cap, the largest bank in the world just moved its gold target higher.

JPMorgan Chase (JPM) raised its 2026 forecast from $5,055 an ounce to $6,300, even after last month’s 11% pullback — a drop that ranks among the sharpest in modern gold history, comparable to declines in 1980 and 1983.

The bank’s view hasn’t changed. “Even with the recent near-term volatility, we remain firmly bullishly convinced in gold over the medium term,” its analysts wrote, pointing to what they describe as a structural shift in capital toward real assets.

The bigger call is even more striking. JPMorgan outlines a path to $8,000–8,500 gold if household allocations rise modestly.

Private investors currently hold about 3% of portfolios in gold. A move to 4.6%, they estimate, would create meaningful new demand in a market already constrained by limited mine supply and steady central-bank buying.

By historical standards, gold ownership remains low. Western investors on average hold less than 1%.

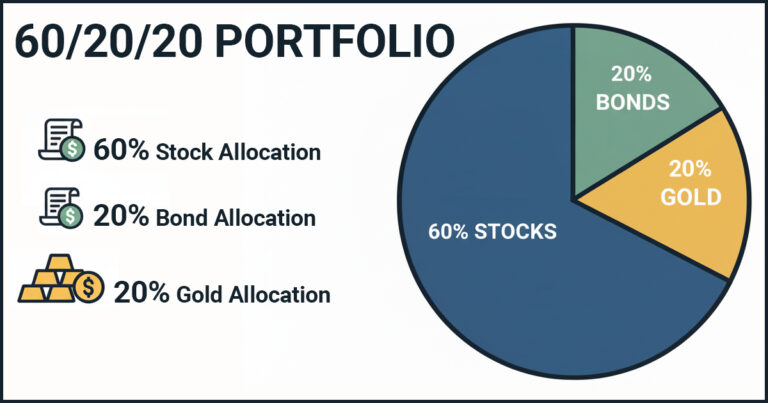

Last fall, Morgan Stanley’s chief investment officer Michael Wilson suggested rethinking the traditional 60/40 stock-bond mix in favor of a 60/20/20 model, with 20% allocated to precious metals.

According to CNBC, JPMorgan strategist Nikolaos Panigirtzoglou said households are substituting “duration risk” in bonds with gold exposure — a shift away from yield sensitivity toward purchasing-power protection.

Courtesy: Sbcgold.com

Courtesy: Sbcgold.com

Central banks are reinforcing that trend. Net purchases have doubled since Russia’s 2022 invasion of Ukraine, as reserve managers diversify away from the dollar.

Gold is up more than 170% over the past five years. JPMorgan argues the drivers behind that move — reserve diversification, inflation concerns and fiscal strain — are not exhausted.

We’ll see how that thesis lines up with the latest market action below…

Today’s session: Equities are selling off hard as energy prices spike and inflation expectations reset. The surge in WTI crude — up 6.35%, near $77 per barrel of WTI — underscores how precarious supply risk has become, and it’s feeding through to risk assets from tech stocks to crypto.

As for the three major U.S. stock indexes, each is down about 1.5% with the Dow, S&P 500 and Nasdaq at 48,200, 6,785 and 22,400 respectively.

The price of gold today suggests the dollar’s strength and rate expectations are moderating safe-haven demand. The yellow metal, in fact, is down 3.95% to $5,103.60 per ounce. At the same time, silver is getting hammered: down almost 7% to $82.65. (Buying opportunity!)

As for digital assets, Bitcoin and Ethereum are down 1.30% and 3% respectively; at the time of writing, priced at $68, 250 and $1,975.

![]() Critical Minerals: Optimus Prime

Critical Minerals: Optimus Prime

“If you are bullish on Optimus and the future of robotics, you are a mining bull too. You must be, because without these weird metals, none of it can happen,” says Paradigm editor and resource-investing expert Matt Badiali.

Tesla began mass production of its Optimus humanoid robot at its Fremont factory on Jan. 21 this year. Elon Musk has committed to selling them to outside customers by 2026 — eventually, a million units a year. The rollout is no longer hypothetical.

Optimus, however, requires a staggering list of raw materials: tin, manganese, copper, dysprosium, lithium, cobalt, terbium, graphite, tantalum and more. “The bad news,” Matt notes, “is that few of these come from the U.S.”

- Tin: Recycled only, no mined supply

- Dysprosium and terbium: No domestic production

- Manganese, graphite and tantalum:

And China controls most of it. “China mines or refines the bulk of these metals,” Matt writes. “China built that industry out over a decade or more. And so it holds the keys to those metals today.

“China boxed out the world, so everyone else is spending whatever it takes to catch up.” When demand soars and supply doesn’t follow, prices go up — and right now, demand is soaring. “As investors, we need to jump on that train. It’s a great way to make money.

“The disconnect for investors,” Matt says, is “they all want to own Tesla, but don’t know a thing about the companies that produce the materials needed for the Optimus program.

“If you are a tech bull,” he concludes, “it makes sense to invest in the metals that drive the development and production of technology.”

![]() AI Bros Are Butthurt

AI Bros Are Butthurt

There’s a strange social expectation surrounding the AI boom: Not only must we accept it, we must rally round it.

“I can’t really remember a boom with such active hostility to it,” says William Quinn, co-author of Boom and Bust: A Global History of Financial Bubbles.

Quinn contrasts AI with past breakthroughs like electricity and automobiles, which stirred fear, yes — but also wonder. AI, he suggests, is “notable, perhaps unique, for the lack of enthusiasm.”

(Mr. Quinn might profit from a brief detour into the early 19th century — specifically, the chapter that introduced the word “Luddite” into the English language. But I digress.)

Nvidia CEO Jensen Huang — with a net worth of $164.1 billion — says criticism of AI has been “extremely hurtful,” arguing the technology is taking “a lot of damage” from “doomer” narratives.

Sam Altman has similarly expressed frustration at what he sees as surprisingly slow “diffusion” and “absorption” of AI into daily life.

The hesitation isn’t imaginary. A 2025 Pew Research survey found about 60% of Americans want more control over how AI is used in their lives, while just 17% are comfortable with it being concentrated in the hands of a few tech billionaires. (Honestly, that much?)

Even more telling: Industry estimates suggest that by mid-2025, only about 3% of global AI users were paying for premium AI services.

If this is a revolution, it’s a very bumpy one. And when even the users won’t open their wallets, maybe the problem isn’t insufficient gratitude — it’s simply unresolved doubt.

![]() AI vs. a Six-Figure Invoice

AI vs. a Six-Figure Invoice

“My company has been using Perplexity.ai to disentangle the international regulatory framework that makes it difficult to export radioactive substances from Australia to an overseas company,” writes a new contributor — in response to Saturday’s 5 Bullets roundup issue: “America’s ChatGPT Map Tells a Story.”

It’s not just who is using AI… It’s why.

It’s not just who is using AI… It’s why.

Click to view the interactive map

“We have been totally amazed by the clarity and depth of the information this has provided my company,” he continues. “We have saved weeks of research and high-competence work.

“Had we hired one of the major consultancies and international law firms, we could have incurred a six-figure invoice for a result that would likely be inferior.

“AI is clearly a massive productivity revolution.”

Emily: We dare not ask which radioactive materials… Thanks for writing in!

Yes, AI can dismantle export controls, draft legal briefs and compress weeks of research into an afternoon. But revolutions are rarely judged on capability alone.

They’re judged on whether ordinary people feel empowered by them… or replaced by them. The verdict is still pending.

Take care, reader! Join us tomorrow for another round of 5 Bullets.

")

")

")

")

")

")

")

")