Oil Shock 2026

![]() Oil Shock 2026 (And a ’70s Flashback)

Oil Shock 2026 (And a ’70s Flashback)

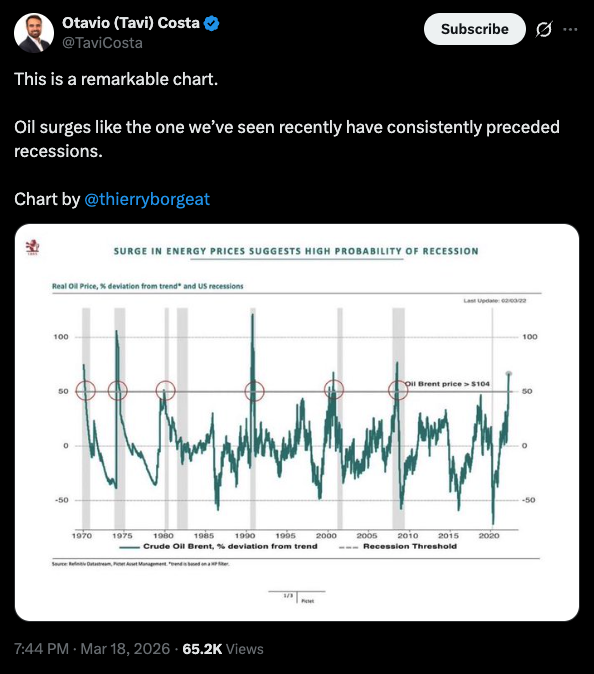

Your editor’s day began with an eye-popping chart sent from six time zones away by Rude Awakening editor Sean Ring. Look closely.

Your editor’s day began with an eye-popping chart sent from six time zones away by Rude Awakening editor Sean Ring. Look closely.

The green line depicts the volatility or lack thereof in oil prices over time. Big swings higher have heralded the onset of nearly every recession — the vertical gray bars — for close to 60 years.

The only exception is the brief COVID recession of 2020 — and even there, you can see it came close. No one remembers now, but oil prices nearly tripled between early 2016 and the autumn of 2018. And a 2020 recession was likely in the cards even without the virus.

We caution: This chart is not a lead-pipe cinch guarantee that a recession is nigh.

In recent years, the economic disruptions wrought by COVID lockdowns have scrambled any number of economic indicators that for decades looked like sure things.

For instance, we had an “inverted yield curve” — in which longer-term interest rates were lower than short-term rates — for a two-year stretch between 2022–2024.

Recessions typically set in less than a year after the curve “uninverts” and once again longer-term rates are higher than short-term rates.

Not this time: While the economy feels punk for anyone other than the top 10% of income-earners, there’s no evidence of a recession as most economists would describe it.

Still… it’s not too soon to start thinking about analogs to the “oil shock” of 1973–74… and the “stagflation” that marked the rest of the 1970s.

At least one economist thinks it’s inevitable…

To refresh your memory: The U.S. government intervened on the side of Israel during the Yom Kippur War of October 1973 — a 19-day conflict between Israel and a coalition of Arab states.

Arab oil producers responded with an embargo on oil sales to the United States. Oil prices quadrupled from roughly $3 a barrel to $12.

The impact was instant and severe: The U.S. economy tumbled into a recession the following month and it dragged on through all of 1974 and into early 1975. Unemployment peaked at 9% (at a time when unemployment was still measured honestly).

It was the worst hit to the economy since the Great Depression of the 1930s.

And even when the recession was over, the recovery was weak. At the same time, reckless money printing by the Federal Reserve aimed at ensuring Richard Nixon’s reelection in 1972 set the country on an inflationary course for the rest of the ’70s, with consumer prices leaping 14% year-over-year by early 1980.

Stagnation + inflation = stagflation.

The stock market was already in trouble during 1973 and wound up falling 45% peak-to-trough over a two-year stretch. It languished into the early 1980s and inflation ate into whatever meager returns the market generated.

Gold, meanwhile…

Well, we might as well give that its own bullet — given the carnage today.

![]() Gold… and 1974… and 2008

Gold… and 1974… and 2008

The good news for precious metals bulls is that the gold price is still in the green year-to-date.

The bad news is that it’s down $216 or 4.5% as we write, barely holding onto the $4,600 level.

Silver is now in the red for 2026, the bid down nearly five bucks on the day to $70.39. The HUI index of mining stocks is down 7.2%, slipping below 700 and basically back to where it was at the start of the year.

We’ll note here that amid the 1973–74 oil shock, gold fulfilled its role as a hedge against geopolitical risk — tripling from $64 to nearly $200 in very short order.

And then it collapsed 50% during 1974… finally, roaring 8X higher by early 1980. Volatility.

Maybe the stronger analogy right now is 2008.

“Back then, fear drove gold and silver down 25% and 55% respectively,” recalls Paradigm natural resources authority Matt Badiali.

“And when metal prices fall modestly, mining stocks collapse. In 2008, the VanEck Gold Miners ETF (GDX), the benchmark for gold mining stocks, fell 70%.”

A falling gold price now? That reflects fear that the Iran war will metastasize into a global economic crisis. Economic fears trump geopolitical fears, at least right now.

Now the rest of the 2008 story: ”Gold and silver bottomed in November 2008,” Matt recalls.

“Gold rose over 150% from its 2008 low to its 2011 high. Silver soared 400% from its 2008 low to its 2011 high. Gold stocks, as tracked by the GDX, rose 250% over that same period.

“We’ve seen this play out before. We’re watching this decline in metal prices as a prelude to another big run. As the miners’ prices fall, we’ll be looking for an entry point. Other less experienced investors will be running for the hills and we’ll be backing up the truck.”

![]() Stocks and Oil: The Market Meltdown That Wasn’t

Stocks and Oil: The Market Meltdown That Wasn’t

What first looked like a rocky day for the U.S. stock market (down) and oil (up) has turned into… well, something rather different.

When we left you yesterday, Israeli airstrikes lit up Iran’s massive South Pars natural gas field — and Tehran was threatening revenge on energy infrastructure in the gulf sheikdoms.

Tehran has since made good on those threats — striking the Ras Laffan liquefied natural gas plant in Qatar, the largest plant for LNG exports in the world. Just like that, an estimated 3.5% of global LNG capacity is gone — and by one ballpark guess, so is a third of global helium supply.

The plant took 14 years to build and Reuters reports that getting it back online will take three–five years.

Iranian forces also targeted the Yanbu oil export terminals in Saudi Arabia. Yanbu is located on the Red Sea and as such is the only way the kingdom’s oil exports can bypass the Strait of Hormuz.

The initial market reaction was stocks down big and oil up big. But as midday approaches on the U.S. East Coast, those moves are looking much more muted.

At last check the S&P 500 is down a little over a half percent to 6,586 — basically a four-month low. Both the Dow and the Nasdaq have shed about three-quarters of a percent. Not great, but not a big whoosh.

➢ Lest we forget: To no one’s surprise, the Federal Reserve left short-term interest rates alone yesterday at the conclusion of its March policy-setting meeting. Looking at the activity in the futures markets, traders now expect no rate cuts this year.

The action in oil, meanwhile, has been simply ridiculous. The “spread” between West Texas Intermediate crude (the U.S. benchmark) and Brent crude (the global benchmark) has blown out to crazy-wide levels. Brent is usually priced higher but at last check it’s $109.74 while WTI is still $98.66.

You don’t have to search far on social media to find still more complaints of market manipulation. Manipulation or no, the spread hasn’t been this wide since mid-2022.

Back to the Strait of Hormuz for a moment: We ran across an observer on X asking why doesn’t Israel’s military act to force the waterway back open.

Answer: The U.S. government guarantees an energy supply to Israel no matter what. That’s according to a 2003 Guardian article that’s resurfaced on social media in recent days…

In 1975, [Secretary of State Henry] Kissinger signed… a memorandum of understanding whereby the U.S. would guarantee Israel’s oil reserves and energy supply in times of crisis… The memorandum has been quietly renewed every five years, with special legislation attached whereby the U.S. stocks a strategic oil reserve for Israel even if it entailed domestic shortages — at a cost of $3 billion in 2002 to U.S. taxpayers.

There’s no evidence to suggest this agreement has since lapsed or been canceled.

We give the last word for now to Cato Institute foreign policy scholar Brandan Buck…

![]() Comic Relief

Comic Relief

Sign of the times, even before the war…

![]() Mailbag: AI Agents, Emily’s Departure

Mailbag: AI Agents, Emily’s Departure

On the subject of AI agents and the computational power they require relative to chatbots, we heard from a member of our Omega Wealth Circle…

“So how many people can use AI agents before the systems are overwhelmed, either by processing power or electricity?

“I think we are about to face a modern example of the ‘tragedy of the commons,’ where if one person grazed his cattle on land open to all, he did well, but when everyone tries to graze their cattle there, the commons is destroyed.

“I suspect that as more people try to use AI agents, the price is going to go up A LOT. The true cost may be in the thousands of dollars per month, and if they charge that much, then the number of users will not overload the systems. If it does, then the price goes up even more.

“In the case you gave of having your flight cancelled and using agentic AI to take care of all the details of flights, hotels, etc., if it cost $10, just for that event, then millions of people would use it, but if it cost $1,000, then the usage would be much less.

“I am watching this space closely.”

Dave responds: As are we, rest assured.

Maybe agentic AI will be the catalyst for the tech industry to move beyond the business model that’s defined it throughout the 21st century: “If you’re not paying for the product, then you’re the product.”

Of course we’ve been pounding the table about AI and its impact on the power grid for over two years — long before the mainstream caught on.

And there’s another constraint facing AI. We touched on it in early 2025. It’s something the technology sector hasn’t grappled with before — the rising cost of borrowed money.

Interest rates move in decades-long cycles — 40 years up, 40 years down, give or take. IBM’s introduction of the first mass-market personal computer in 1981 coincided almost perfectly with a secular peak in interest rates — 15.8% on a 10-year U.S. Treasury note.

From that peak, it was generally down for the next four decades — not a straight line, of course, but a steady trajectory. The tech industry was able to ride that wave all the way down; any debt they took on for startup or expansion could be refinanced later at a lower interest rate.

But those days are over. The bottom of that falling-rate cycle came in August 2020, when the 10-year T-note yielded a paltry 0.5% (and the work-from-home crowd had just loaded up on all the electronics they’d need for a few years).

Today the 10-year yield rests at 4.26%. It’s higher now than when the Fed started cutting short-term rates 18 months ago. Usually long-term rates fall in sympathy with cuts to short-term rates — but no longer.

Rising rates might be one reason the much-ballyhooed Stargate AI project can’t get off the ground — in addition to infighting among the principal investors.

“Thank you for all you've done, Emily. You, Dave and the team are the best,” a reader writes as Emily Clancy prepares to move on.

“5 Bullets has been my No. 1 must-read for more years than I can count. Good luck with your new venture!”

“Congratulations on your move to join Jim Rickards’ team,” says another note to Emily. “I know you will learn all kinds of new skills and build your knowledge base even deeper than it is today.

“I will miss your contributions to the 5 Bullets. You marry information, perspective and a clever sense of humor. Your unique style is a bonus to the information the emails always contain.

“Best wishes for a wonderful career move.”

Dave clarifies: I gave a longtime reader the wrong impression yesterday. To be clear: When I said I was preparing “my own sendoff” to run in tomorrow’s edition, I meant my sendoff for Emily.

Sorry if I gave anyone a scare! Or in the case of this one reader, inspired him to raise a glass after “being a teetotaler for some time.” (It’s kinda weighing on my conscience now…)

")

")

")

")

")