Pontius Pilate Powell

![]() Pontius Pilate Powell

Pontius Pilate Powell

Fed chief Jerome Powell has begun his farewell tour by saying everything that happens from here on is NOT. HIS. FAULT.

Fed chief Jerome Powell has begun his farewell tour by saying everything that happens from here on is NOT. HIS. FAULT.

From the front page of today’s Wall Street Journal…

Federal Reserve Chair Jerome Powell said Monday the central bank is inclined to hold rates steady and look past the energy shock from the war in Iran but cautioned that it might not be able to sit on the sidelines if rising prices shift the public’s expectations about inflation over time.

Powell, speaking to students at Harvard University, laid out the textbook case for patience: Energy disruptions tend to be short-lived, and monetary policy works too slowly to counteract them in real-time. He added a critical caveat, however, by noting how five years of above-target inflation made it harder to assume the public would simply shrug off another round of rising prices.

“You can have a series of these supply shocks and that can lead the public generally — businesses, price setters, households — to start expecting higher inflation over time. Why wouldn’t they?” Powell said.

On the one hand, Powell is right. Monetary policy can’t offset rising energy prices. It’s that old saying about how the Fed can’t print barrels of oil.

But c’mon. It’s plain as day. Powell is using the Iran war as cover to slough off responsibility for every boneheaded decision on his watch for the last eight years — decisions you’re living with right now.

Powell has about six weeks left as Fed chair — maybe more if there’s a struggle in Congress over the nomination of his successor.

Time flies: The narrative surrounding Powell when he ascended to the chairmanship in 2018 was that he’d be different from his predecessors.

Janet Yellen and Ben Bernanke? They were haunted by the 1930s and the Great Depression — which is why they printed money to a fare-thee-well and kept short-term interest rates pinned near zero for seven years once the 2008 financial crisis reached critical mass.

You wanted safe, reliable income in T-bills or CDs? Go pound sand they said — we’ve got to do a solid for our cronies on Wall Street.

Powell, we were told, was haunted instead by the inflation of the 1970s. He’d be a more responsible steward of monetary policy.

Powell raised short-term interest rates in baby steps for the first several months of his term — until Wall Street threw a hissy fit at the end of 2018, sending the S&P 500 down 20%.

And that was the end of his first rate-raising cycle. It went down in history as the “Powell pivot.”

He started cutting rates a few months later. Then he started printing money anew in the fall of 2019 amid a crisis in financial instruments called repos, or repurchase agreements.

Once more the Fed was riding to the rescue — fixing a crisis made on Wall Street, at the expense of everyday Americans.

Coming barely a decade after the 2008 bank bailouts, there was real potential for a torches-and-pitchforks moment — until COVID conveniently came along.

The Fed could bail out the system once more — this time with the excuse of You don’t want a financial collapse on top of a pandemic, do you?

The rest of the story follows in Bullet No. 2…

![]() Powell’s Inflationary Legacy

Powell’s Inflationary Legacy

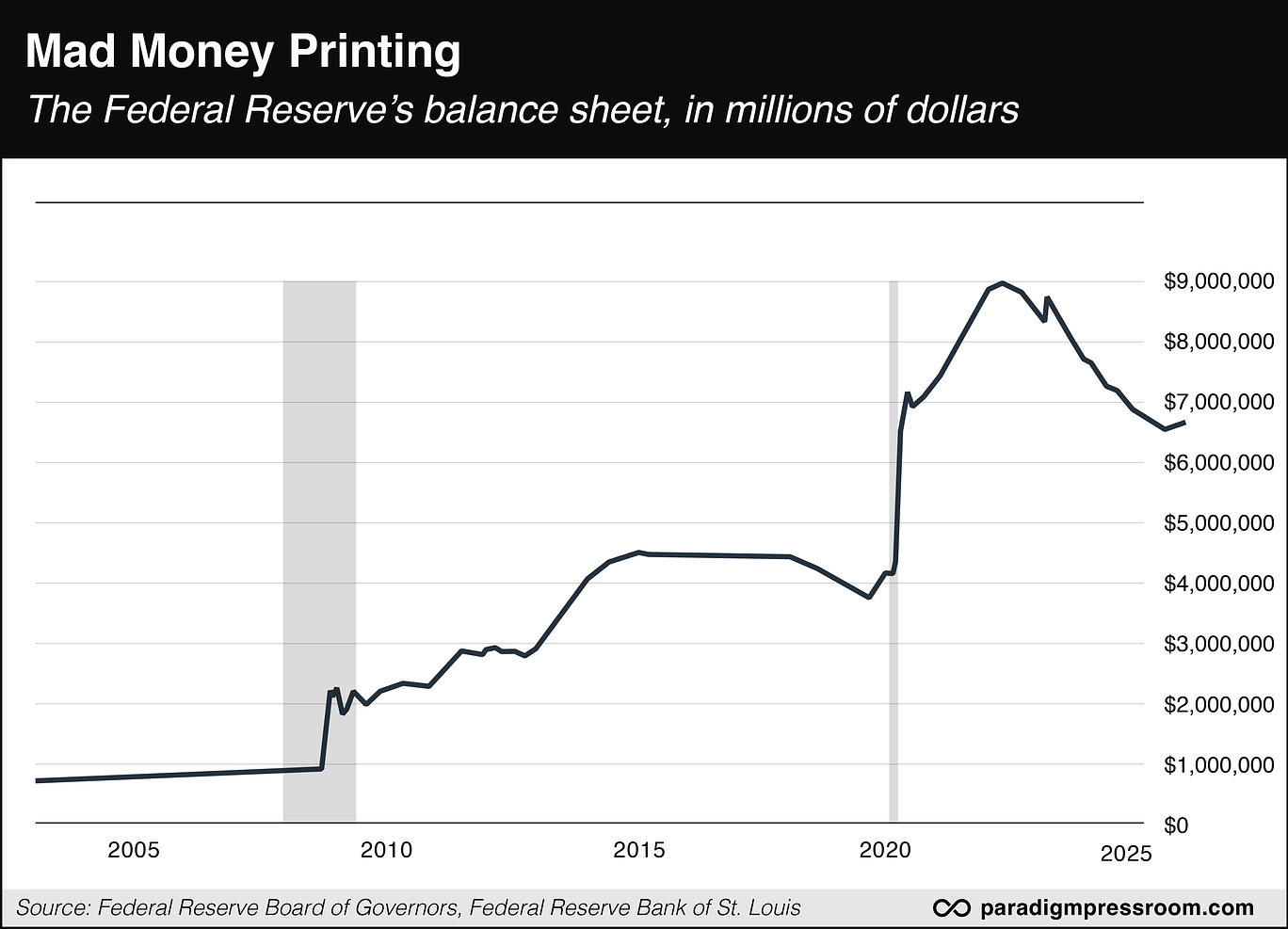

In the 2020s, the guy who supposedly was haunted by the 1970s started following the Fed’s ’70s playbook, page by page.

Powell’s mad money printing from 2020–2022 dwarfed anything Yellen and Bernanke had done in the wake of 2008. Here’s a chart of the Fed’s balance sheet, with both recessions highlighted in the gray bars.

Pressed throughout 2021 about the likelihood that Fed money printing would manifest as consumer price inflation — as happened in the 1970s — Powell was nonchalant.

The official inflation rate sailed higher all year — from 1.7% in February to 6.9% in November. The whole time, the word Powell invoked to describe any inflation was “transitory” — right up to the moment he acknowledged to the Senate Banking Committee that it might be time to “retire transitory” as a descriptor of how the Fed viewed consumer price rises.

To combat the mess he made, Powell embarked on an epic interest rate-raising cycle in 2022 — the steepest in over 40 years.

Yes, that did have the effect of bringing the inflation rate down from its insane 9.0% peak in mid-2022 to a range between 2.3–3.0% in the last year.

But all the price increases of 2021–22? They never reversed. They were locked in permanently.

Worse — and we can’t emphasize this often enough — once inflation sails past 5%, it takes a decade on average to get back to “normal” 2% inflation.

The historical evidence is overwhelming. If you’re hoping for a return to pre-COVID inflation levels, it probably won’t happen until the early 2030s.

But as he saunters off into the sunset, Jay Powell has let it be known: Any inflation you experience from March 2026 onward is strictly a knock-on effect of the war and it’s got nothing to do with him. It’s just supply shocks fueling people’s expectations.

Really, Pontius Pilate’s got nothing on Jay Powell. We’re washing our hands of this thing! Not our problem! We didn’t start the fire!

To be sure, Powell doesn’t bear sole responsibility for the price increases that burden you this decade. There’s Joe Biden… Donald Trump… free-spending congresscritters of both parties…

But for Powell to point a finger at the war and dodge his share of the blame? Just revolting.

[Program note: This might not be the first exercise in Powell-bashing you’ll see in our publications this week. On the Paradigm internal e-chat yesterday, a handful of us got on a roll. Byron King in particular might have a few choice words…]

![]() Team Trump’s Trial Balloon

Team Trump’s Trial Balloon

After hitting their highest levels since 2022, oil prices edged downward overnight thanks to a trial balloon someone in the Trump administration floated to The Wall Street Journal.

Back to the paper’s front page…

President Trump told aides he’s willing to end the U.S. military campaign against Iran even if the Strait of Hormuz remains largely closed, administration officials said, likely extending Tehran’s firm grip on the waterway and leaving a complex operation to reopen it for a later date.

In recent days, Trump and his aides assessed that a mission to pry open the chokepoint would push the conflict beyond his timeline of four to six weeks. He decided that the U.S. should achieve its main goals of hobbling Iran’s navy and its missile stocks and wind down current hostilities while pressuring Tehran diplomatically to resume the free flow of trade. If that fails, Washington would press allies in Europe and the Gulf to take the lead on reopening the strait, the officials said.

Huh. Iran never had much of a navy to begin with. As for its missile stocks, U.S. officials told Reuters this week that it’s likely only one-third has been destroyed with certainty. Tehran is launching fewer missiles than at the outset of the war, but they’re still hitting valuable and seemingly undefended targets.

But as for the main point, the memo-o-sphere is already weighing in…

It’s at this point we have to emphasize: Strictly speaking, the strait is not closed. It’s a selective blockade. Tehran is letting limited traffic through, especially if it’s oil paid for in Chinese yuan instead of U.S. dollars. And Tehran has suggested more traffic might be let through if shippers pay a fee.

All of which contrasts with the fact the strait was freely navigable before Washington and Tel Aviv launched their war.

In any event, the effect of this trial balloon on the oil price was short-lived.

Last night, a barrel of West Texas Intermediate fetched $106. When the Journal published its story online, it instantly plunged to about $101. As we write, it’s back above $104.

Meanwhile, stocks are staging an honest-to-goodness rally — one that will likely stick through day’s end, unlike yesterday. At last check, the S&P 500 is up nearly 1.6% to 6,444. The Nasdaq is up 2%, the Dow about 1.25%. Even small caps are sharing in the cheer, the Russell 2000 up about 1.4%.

Gold might have finally broken through the $4,500 barrier that proved to be overhead resistance for about 10 days — the bid up to $4,619. And silver’s roared over 5% higher to $73.71.

No joy for crypto, though — Bitcoin a little over $67,000 and Ethereum a little under $2,100.

![]() Cost of War Update

Cost of War Update

For the record…

A month into the war, the Iran War Cost Tracker site pegs the taxpayer cost at nearly $37 billion. That’s based on various estimates the Pentagon has informally issued either to Congress or the media — $11.3 billion the first six days, $1 billion a day after that.

Which reminds us of a peculiar line of argument coming from the administration the last 48 hours…

According to the World Bank, Iran spent about 2% of its GDP on the military during 2024. The United States, 3.4%. Projection much?

It’s here we’ll remind you the previous round of forever wars in the Middle East, from 2001–2021, cost $8 trillion. And that’s just the direct monetary cost. The prosperity we gave up along the way? And the costs to our freedoms? Incalculable.

![]() Sympathy Pangs

Sympathy Pangs

Yesterday’s mailbag section brought pangs of sympathy from one reader.

“I feel like the retiree waiting for the ticker so she has a chance to push up that $1,000 nest egg. That’s the whole idea. Is it Dave's prerogative to determine that she should be a more conservative trader?

“One listens to these long videos with the hope you are giving a tidbit and only get this redundant over-and-over long, drawn-out video that ends with buy something.

“I don't remember this when I signed up with Rickards. This group has changed — not sure for the better.”

Dave responds: I hear your frustration. Let me approach this from a different angle — because looking from the inside, I’m not sure what’s changed. Our MO has been the same for the nearly two decades I’ve worked with Paradigm Press and its predecessor firms.

The entry-level publications — Rickards’ Strategic Intelligence, Altucher’s Investment Network — are where the editors usually spotlight companies with larger market caps and a risk profile that’s suitable for someone with limited capital. The recommended hold time is usually months if not years.

The premium publications — such as Rickards’ Insider Intel or Altucher’s True Alpha — frequently entail either options or microcap stocks. The profit potential is greater, usually much greater. The time frame in which those profits could materialize is shorter, sometimes much shorter.

But much bigger profits in a much shorter time frame inevitably involves a greater level of risk.

In the case of our current campaign for Microcap Millionaire… it would be the height of irresponsibility for us to recommend a company this size to over 200,000 Altucher’s Investment Network readers. Doing so would artificially pump up the share price — only to have it sink back to Earth in short order.

Again… the idea is that you have a good experience with an entry-level newsletter, racking up gains that then allow you to step up to a higher level of service, amplifying and accelerating those gains. That’s how we get happy long-term customers. Win-win!

")