Just Another Tuesday

![]() Just Another Tuesday

Just Another Tuesday

And so here we are: The U.S. president threatens “a whole civilization will die tonight” and the U.S. stock market sees it as just another Tuesday.

And so here we are: The U.S. president threatens “a whole civilization will die tonight” and the U.S. stock market sees it as just another Tuesday.

As we write, the president’s 8:00 p.m. EDT deadline remains in place.

We’ll get to the war and the markets in Bullet No. 2. But first…

It’s essential to zoom out and observe the mainstream is catching on to something we’ve warned about for years.

As a reminder, the “petrodollar” arrangement is what emerged in the aftermath of the Arab oil embargo in late 1973 — a response to U.S. support for Israel in the Yom Kippur War. Oil prices quadrupled in a matter of weeks.

The following year, Secretary of State Henry Kissinger midwifed a system under which Saudi Arabia prices oil in U.S. dollars and uses its clout to get other OPEC nations to do the same. In return, the U.S. government protects Saudi Arabia and its allies against foreign invaders and domestic rebellions.

Starting in 1974, anyone who wanted to buy oil needed dollars to do so. The Saudi and other Gulf governments then took those dollars and invested them in U.S. Treasury debt.

The petrodollar greased the wheels of world commerce and underwrote Uncle Sam’s decades-long debt bender.

For more than 10 years, we’ve been chronicling signs that this arrangement was slowly coming apart.

A turning point came in 2022 — after Russia invaded Ukraine and Washington responded with a raft of sanctions aimed at curbing Russia’s energy revenue.

Russia soon began selling oil to China and India in exchange for yuan and rupees. And Saudi Arabian leaders started talking publicly about selling oil to China for yuan.

If 2022 was a turning point, 2026 is the breaking point.

In a Bloomberg opinion column, Aaron Brown — the former head of financial market research at AQR Capital — describes the dynamic of the last 39 days:

Turkey, India, Thailand and other oil-importing nations are caught in a brutal arithmetic: Oil priced in dollars has surged past $100 a barrel while their currencies weaken against the greenback. To limit depreciation — which would push domestic oil prices even higher, forcing either fiscal subsidies or household pain — central banks intervene in currency markets. That requires dollars. The most liquid dollar asset any central bank holds is Treasuries. So they sell.

Result: Foreign central banks have been net sellers of Treasuries for five straight weeks. That’s pushing Treasury prices down and Treasury yields up. The yield on a 10-year T-note was 3.9% when the war began and climbed over 4.4% by late March.

Typically during moments of geopolitical turmoil, Treasuries are a safe haven for scared money. No more. Brown again:

The flight-to-quality trade has always rested on a political premise: That in a global crisis, the United States is a stabilizer or bystander, not a combatant. But the calculus changes when the U.S. itself is the belligerent; when the conflict is partly America’s war, driving the oil shock, straining Gulf relationships and generating the fiscal pressure that has bond investors worried about U.S. budget deficits. Not completely. Not permanently. But enough.

It was inevitable. If it wasn’t the Iran war, it would be something else. Interest rates tend to move in long 80-year cycles — 40 years up, 40 years down.

They’ve been headed up since the summer of 2020 — not in a straight line, but the trajectory is in place. Long-term Treasuries are no longer a safe haven. (Your editor ditched all his long-term Treasury holdings in 2024 once it was clear 2020 marked the bottom in rates.)

Gold fulfills the safe-haven role from here. Yes, it’s taken a tumble in recent weeks. That too is a function of the global dash for liquidity Brown describes above. “Weak hands” are selling. Strong hands are scooping up a (relative) bargain, getting ready for the next phase up.

![]() Countdown

Countdown

Amid Donald Trump’s latest threats, a barrel of West Texas Intermediate is up nearly four bucks, over $116.

We must caution once more: That’s just the futures price. Real barrels for export to oil-starved customers overseas are fetching much higher prices.

The post above prompted the following reply from a self-described “captain of an offshore drilling asset”:

The physical market is telling a much different story than paper. The scary part is that markets don’t seem to care right now. It really feels like Feb of 2020 all over again. You could see the world shutting down yet everyone in the U.S. just turned a blind eye to it.

“The last ship from Hormuz is arriving in Europe in three days,” says a tweet from commodities analyst Lukas Ekwueme. “In the U.S., eight days. Australia in two weeks.”

If the Strait of Hormuz reopened today, it would take at least 40 days before any more oil comes into port.

“What we’re seeing now is still the front edge of the shock,” Ekweume concludes. “The full extent of the supply shortfall hasn’t even hit yet.”

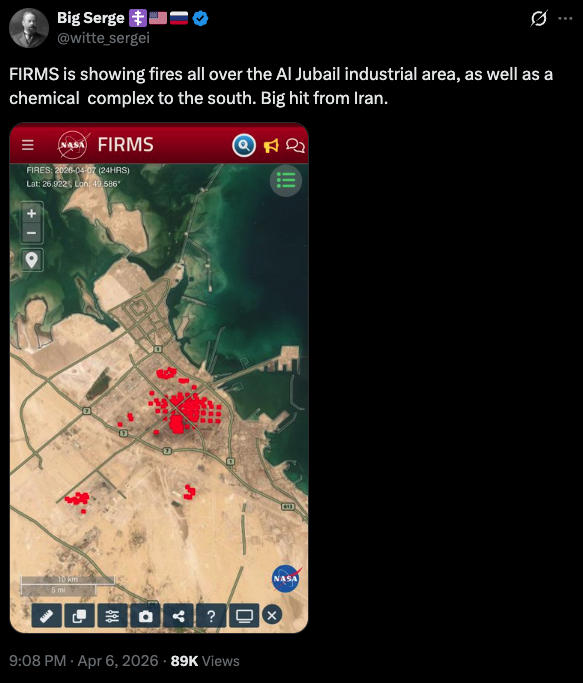

And the war grinds on as the deadline approaches: After U.S. and Israeli airstrikes on an Iranian petrochemical hub, Tehran hit back — hard.

Iranian airstrikes torched the kingdom’s Jubail petrochemical facility — which accounts for 7% of Saudi Arabia’s total economic output.

There’s considerable doubt about the provenance of the video footage accompanying most of the social media posts about this attack. The Gulf sheikdoms have been cracking down hard on video footage of attacks on their countries.

NASA’s fire-mapping platform called FIRMS, on the other hand, is more reliable…

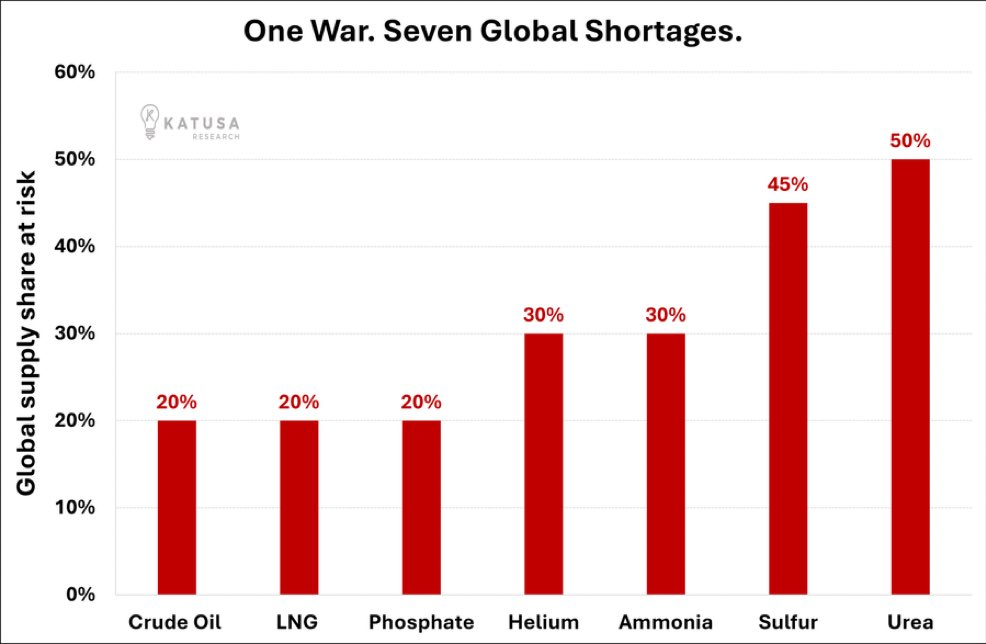

Meanwhile, on the Paradigm Press mobile app, our own Byron King spotted a chart from Katusa Research that reminds us the supply squeeze isn’t just about oil…

The stock market reaction seems to be one of “fearing the worst and hoping for another Trump TACO.”

At last check, the S&P 500 is down 0.8% at 6,557. The Dow’s losses are narrower, the Nasdaq’s steeper.

Gold is steady at $4,646 but silver has shed nearly two bucks to $70.62. No excitement in crypto — Bitcoin a little under $68,000 and Ethereum at $2,070.

![]() Medicare Climb-Down

Medicare Climb-Down

The health insurance stocks are defying today’s modest sell-off — because of a climb-down by the Trump administration.

In January we told you the administration was proposing to hold its 2027 compensation for Medicare insurers at 2026 levels. The announcement hammered the share prices of UnitedHealth and other big companies providing Medicare Advantage plans.

But that was just a proposal and not a final announcement. The final announcement came after the market close yesterday: Next year’s payments will be 2.48% higher.

That’s nowhere near the 4–6% that Wall Street analysts were counting on at the beginning of the year — but it’s enough to send UNH shares up 8% today, and CVS nearly 5%.

Why the change of heart by the administration? “We have to be wise stewards of the tax dollar,” says Medicare program director Chris Klomp — but “we need to make sure that plans aren’t pulling out of markets, that they’re not cutting benefits that beneficiaries are relying on,” he tells The Wall Street Journal.

Well, OK. But this issue will rear its head again next year. And the year after that.

Something’s got to give, eventually. The U.S. health care system is ruinously expensive — consuming 35 cents of every dollar spent by the federal government.

Our guidance from January stands: If you’re on a Medicare Advantage plan right now — more than half of Medicare beneficiaries are — it’s not too early to start thinking about what your world will look like if the system can no longer sustain these plans and your only option is a more costly Medicare supplement or “Medigap” plan.

![]() Comic Relief

Comic Relief

We get our yuks where we can find them…

![]() Mailbag: Tough Jobs, Propagandists

Mailbag: Tough Jobs, Propagandists

“Dave, as usual your response to my note was very well said,” a reader writes back after the mailbag in yesterday’s edition.

“I know that you guys have a very tough job in helping investors maximize their returns without setting them up to take massive losses when markets shift. I think you guys do it better than almost any other investment service I’ve encountered but don’t quote me on that because I don’t have the data to back it up 😉.

“You’re very good at your job and I get lots of value from your missives so I hope that you plan to continue (as I do as long as I think I still bring value) for some years yet.”

“Mr. Gonigam, I’ve noticed a concerning trend in the X accounts you choose to highlight in your daily newsletter,” a reader writes.

“It took me a couple minutes to swipe through Brandon Weichert’s X feed to realize he is a hack and media propagandist. Not the worst by any means, but he reposts garbage accounts that push misleading and hyperbolic narratives. It’s a credibility issue.

“But we can’t follow the likes of Loomer, Bongino and now Hannity for fear of falling into a closed loop of information gathering. I understand the shortcomings of MAGA and political idolatry, but the American political system is broken. Progressives took over the Democrat party and their policies have destroyed a debt-laden West. We have to choose sides. I’ll never vote Democrat again, and Democrats will never vote for a Libertarian. I don’t think they are well versed in Mises or Tocqueville.

“Trump was an extreme choice, but the fatal flaw in party politics is you have to pick somebody who can win. We are stuck, at least until the union breaks apart; or election outcomes become compulsory and predetermined.

“In the meantime I will support and follow those who rightfully skewer the progressives and radical left. Which at times has been Mr. Gonigam himself! That’s when I like him best.”

Dave responds: Well, thank you. To address your first concern: Even hacks and propagandists have a worthwhile point to make now and then.

Everyone’s mileage will vary but I can’t bring myself to take sides. If we’re to take the president at his word, he’s on the verge of taking a catastrophic step tonight or tomorrow. And rather than put up any resistance at a moment it’s most needed… the Democrats are standing aside so they can win the midterms.

We’ll give the final word today to Charlie Kirk, from the grave…

")

")