The FDIC Fouls Up

- “Accountability” for bank failures

- A quiet stock market (Too quiet?)

- Follow-up file: Internet censorship lands at SCOTUS

- A uniquely Japanese problem (for now)

- Mailbag: Mad COVID spending and “massive change”

![]() “Accountability” for Bank Failures

“Accountability” for Bank Failures

The FDIC has issued an “after-action report” on its conduct in the years before the collapse of First Republic Bank — the second-largest bank failure in U.S. history. We can summarize it in one word: Oopsie!

The FDIC has issued an “after-action report” on its conduct in the years before the collapse of First Republic Bank — the second-largest bank failure in U.S. history. We can summarize it in one word: Oopsie!

In the report’s own words, regulators “could have been more forward-looking” as they analyzed the risk of rising interest rates to the bank’s bond portfolio. They “could have done more” to goad bank management to get their act together. They were “too generous” in their estimates of the bank’s liquid assets on hand.

As with the failure of Silicon Valley Bank, rising interest rates did a number on First Republic’s bond holdings before its collapse on May 1. And by the same token, First Republic could have hedged that risk with interest-rate swaps, but chose not to do so because that would have cut into profit margins.

As it happens, a bank with a similar name appears to be staring down the same scenario.

Republic Bank — the banking unit of Republic First Bancorp — holds $6 billion in assets and has 35 branches in Pennsylvania and New Jersey.

“There may be a lesson here,” write Pam Martens and Russ Martens of Wall Street on Parade: “don’t put the word ‘Republic’ in the name of your bank; don’t hold a lot of uninsured deposits; and don’t have wads of unrealized losses on your investment securities.”

Republic Bank’s SEC filings are not current… but the Martenses spotted the following disclosure in one of its quarterly reports from last year: “As of Sept. 30, 2022, our 100 largest bank depositors accounted for, in the aggregate, 16% of our total deposits. The majority of these deposits are not insured by the FDIC and could present a heightened risk of withdrawal, if such depositors materially decreased the volume of those deposits, it could reduce our liquidity.”

Shares of Republic First Bancorp (FRBK) have plunged 96% in a year. The Nasdaq delisted those shares last month; they trade over-the-counter this morning for 18 cents.

Even mainstream media are zeroing in on banks that appear to be in trouble based on public filings.

This week the San Antonio Express-News had a lengthy write-up on Industry Bancshares — based in the Houston suburb of Industry and with 27 branches under six different subsidiaries.

“Since at least December and through the latest public filing of financial data in June, all six reported a significant negative net worth using traditional accounting standards.”

Again the story is the same — big losses in the bank’s bond holdings, and a huge amount of uninsured deposits.

![]() A Quiet Stock Market (Too Quiet?)

A Quiet Stock Market (Too Quiet?)

“It's getting quiet out there... really quiet,” says Greg Guenthner of Paradigm’s Trading Desk.

Greg directs our attention to recent research from Schwab: “The S&P has now gone 140 trading days without moving at least 2% up or down. This is the second-longest ‘low-vol’ stretch in 15 years -- the most recent one being the slow and steady rally from 2017.”

Even though the stock market is on track to end the week in positive territory, “I’m not feeling particularly bullish. Not in the short term.”

Sure enough, the S&P 500 is down nearly 1% on the day to 4,462. Once more, the index is no better off now than it was two months ago. The Dow is holding up a little better, while the Nasdaq is faring worse.

Reasons? Who knows. Unless you get a move of 2% or more in either direction, there’s never an obvious explanation. Mainstream financial media frequently try to serve one up, but even CNBC isn’t trying today: “Dow slides 200 points as it closes out volatile week ahead of Fed decision.”

Hmmm… Maybe Jim Rickards’ outlier forecast that the Federal Reserve will bump interest rates higher next Wednesday is slowly rippling through Wall Street?

If it happens, it would trigger a shock wave, that’s how unexpected it is. Perhaps even a 2% down day for the S&P.

True, there are other factors casting a pall over the market: The auto workers’ strike is underway and the chances of avoiding a partial government shutdown at the end of this month are almost nil.

One economic number of note: Industrial production rose 0.4% in August. Not a huge surprise, but also more than expected. It’s one more data point reinforcing Jim’s thesis that the economy is too hot for the Fed’s liking and another rate hike sooner rather than later is needed to rein inflation back in.

Crude is up another 53 cents to $90.69. Precious metals are rallying to end the week, gold up to $1,926 and silver to $23.20.

![]() Follow-up File: Internet Censorship Lands at the Supreme Court

Follow-up File: Internet Censorship Lands at the Supreme Court

It appears Missouri v. Biden — aka the social-media censorship case — is racing up the Supreme Court docket.

When last we left the story on Monday, a three-judge panel of the U.S. Fifth Circuit Court of Appeals ordered the White House, Surgeon General, CDC and FBI to stop pressuring the Big Tech companies to censor posts that run counter to Biden administration narratives.

To no one’s surprise, the Biden administration appealed the ruling yesterday. In response, Supreme Court Justice Samuel Alito temporarily paused the Fifth Circuit’s order until Sept. 22, one week from today.

Alito also gave the lead plaintiffs in the case — the attorneys general of Missouri and Louisiana — until next Wednesday to respond.

Jenin Younes — the courageous lawyer from the New Civil Liberties Alliance who represents several of the private-sector plaintiffs — expects the case won’t be dragged out indefinitely.

If you’re a newer reader, and you’re not fully up to speed on the case and the stakes, you might wish to review the latest edition of what’s become our annual censorship issue, published each August.

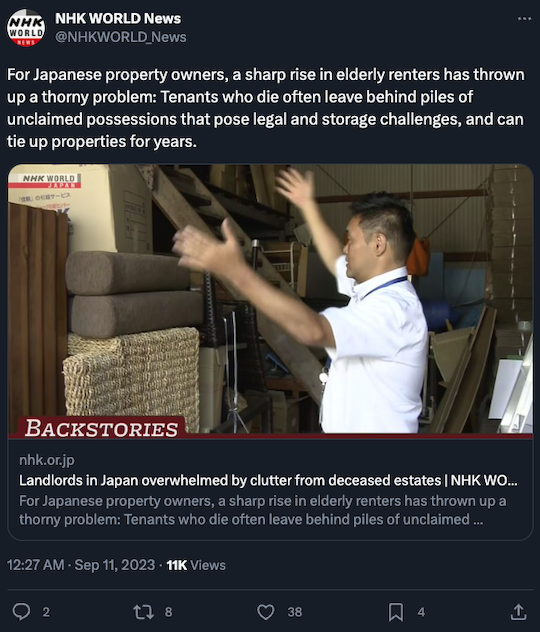

![]() A Uniquely Japanese Problem (For Now)

A Uniquely Japanese Problem (For Now)

Here’s an unexpected consequence of Japan’s demographic difficulties…

Imagine being the landlord of an elderly tenant who dies. You can’t track down next of kin. Without permission from next of kin, the law says you can’t get rid of the deceased’s belongings. So you have to stash them in a storage unit, at your expense of course.

Apparently this is happening in Japan a lot, according to a story from the state broadcaster NHK: “A representative of a property management firm in Fukuoka City gestures around a warehouse cluttered with TVs, fridges, tables, chairs and other items. ‘This is all from the homes of people who died,’ he says. ‘We can't throw any of it away without permission.’”

And this corporate landlord can count itself lucky. But for mom-and-pops? “The situation is worse still for owners who can't afford storage space and are forced to keep belongings in their properties while they search for heirs, sometimes for years, making it impossible to sign new tenants in the meantime.”

The problem is so widespread that many landlords refuse to rent to elderly tenants unless those tenants have a guarantor. "Many people who have no relatives, or who are estranged from their relatives, find it hard to get approval for a rental," says Matsuda Akira — who runs a nonprofit that tries to link up such people with housing.

What’s happening in Japan probably won’t stay in Japan. Much of Europe is on track for a similar aging-out of the population; it’s just a few years behind. At least on this score, the United States will fare better than the rest of the developed world.

![]() Mailbag: The Mad COVID Spending… and Paradigm’s “Massive Change”

Mailbag: The Mad COVID Spending… and Paradigm’s “Massive Change”

“I can only laugh at Sen. Warren pleading with Janet Yellen about high interest rates threatening the financial system,” a reader writes after yesterday’s edition.

“I guess Elizabeth never learned there are two inflationary forces when meddlers run the economy: 1) Monetary policy courtesy of the Federal Reserve, and 2) Fiscal policy courtesy of Elizabeth and her ilk.

“Perhaps if Congress would stop spending money with abandon the Federal Reserve might be able to reduce rates. Hello? Liz? … anybody home?”

Says another: “Since Elizabeth Warren was, dare I say, on the warpath not long ago advocating the COVID lockdowns now impacting commercial real estate, maybe she shouldn't be offering advice to anyone.”

Dave responds: Lockdown really is the gift that keeps on giving. There is so much we are contending with in the economy and the markets that wouldn’t be happening without it.

According to figures from the Office of Management and Budget, total federal spending in the pre-COVID year of 2019 was $4.45 trillion. In 2020 it zoomed up to $6.55 trillion, peaking at $6.82 trillion in 2021.

Yes, it backed off in 2022 to $6.27 trillion and the 2023 total is on track for about $6.37 trillion.

So… even though Joe Biden has rescinded the COVID emergency orders issued by Donald Trump — that’s how the unvaccinated Novak Djokovic was able to compete in the U.S. Open this year — federal spending is now 43% higher than it was pre-COVID.

There’s no going back to any sort of pre-COVID “normal” as far as the federal budget goes. The COVID-era increases are permanently baked in. That’s why inflation is back on the rise, why interest rates have begun a multi-decade climb… and why the banks are once again in trouble.

“This ‘massive change’ happening within your company is exaggeration,” a reader writes in response to one of our recent (and more popular) sales promotions. “It’s pure hyperbole and a waste of my time.

“I watched the video. So what, that now your staff can make trades and recommend them to us. Big freaking deal. Heck, I wouldn't even know if you hadn’t told me. Will it affect how I trade? Not at all. When you use exaggeration like you do with this announcement, it just makes me wonder where else you're using hyperbole. It tarnishes your reputation.”

Dave responds: Hmmm… Perhaps, at least for you, we didn’t convey the significance of this change. So I’ll try it here.

For a long time, it was company policy that our editors could not own a position in the securities they recommend to you.

We felt it important to keep church and state separate, as it were. We wanted to avoid any appearance of conflict of interest. We sought to erase any perception that an editor was padding his account simply because his readers were buying into positions he already owned.

But within recent months, and after a great deal of soul-searching (including reader feedback), we had a change of heart.

In the end, we concluded it would give our editors more credibility in the eyes of our readers if they could eat their own cooking. In such cases, it’s not just your money on the line, it’s theirs. You win when they win — and vice versa. Of course, we furnish full disclosure if an editor owns a position in one of his or her recommendations.

So yes, we do think it’s a massive change. One of our most popular trading services of 2023, Zach Scheidt’s Income Alliance, could not exist without it.

Zach has put $100,000 of his own family’s money into a trading account. In that account, he executes every single trade that he recommends to his readers — giving them a 15-minute head start, just to be totally fair about it.

As we mentioned a few days ago, Zach can generate up to a month’s worth of income in his personal account in as little as 48 hours — $6,494 in four days… $10,617 in six days… even $13,204 in two days.

And when he prospers, readers prosper — like an 82-year-old retiree named Mary who’s using the proceeds from this strategy to help a granddaughter pay for tuition at Stanford.

So… that’s the background behind our “hyperbole.” Thanks for the opportunity, dear reader, to spell it out in a little more detail — and for a gentle reminder that reader trust is something we must strive to earn on a daily basis.